04 March 2025

By Maynard Paton

FY 2024 results summary for Bioventix (BVXP):

- A record FY, showing revenue up 6% and profit up 5%, although the 3p per share reduction to the H2 dividend illustrated a below-expectations performance following an unfortunate troponin-royalty error.

- Sales progress was very mixed, with best-seller vitamin D up just 1%, the now “mature” troponin up only 3%, the once-popular testosterone down 29%, 30-year-old T3 up 21% and general Chinese royalties becoming “more significant“.

- R&D revenue of £155k, the commencement of “large-scale production“, promising snippets from scientific papers alongside ongoing Quanterix promotion suggest BVXP’s Alzheimer’s work has increasing potential to become a substantial commercial success.

- The wonderful economics of the antibody portfolio continue, as this FY displayed a majestic 78% operating margin, a super £800k revenue per employee, net cash equivalent to a hefty 44% of revenue and capex of just £16k.

- The £30 shares currently trade at their lowest P/E since 2016, offer a 5%-plus yield for the very first time and might value the Alzheimer’s R&D at a very pessimistic zero. I continue to hold.

Contents

- News links, share data and disclosure

- Why I own BVXP

- Results summary

- Revenue, profit and dividend

- Royalty income and physical sales

- Vitamin D

- Troponin

- Other core antibodies

- Alzheimer’s R&D: revenue

- Alzheimer’s R&D: neurodegeneration and brain-derived tau

- Alzheimer’s R&D: amyloid plaques and pTau

- Alzheimer’s R&D: tau tangles and detector antibodies

- Other R&D

- Financials: margin and employees

- Financials: balance sheet and cash flow

- Valuation

News links, share data and disclosure

- Annual results and presentation for the twelve months to 30 June 2024 published 28 October 2024;

- ShareSoc seminar hosted 27 November 2024, and;

- AGM attendance on 05 December 2024.

- Share price: £30

- Share count: 5,219,656

- Market capitalisation: £157m

- Disclosure: Maynard owns shares in Bioventix. This blog post contains ShareScope affiliate links.

Why I own BVXP

- Develops diagnostic blood-test antibodies, substitution for which can be limited due to protracted regulatory testing that in turn can lead to revenue continuity for a decade or two.

- Boasts founder/entrepreneurial chief exec who has overseen an attractive growth record, prefers a cash-rich balance sheet, retains a 6%/£9m shareholding and has declared seven special dividends.

- Employs ‘scalable’ royalty model that requires few employees and leads to terrific margins, generous cash flow and immense returns on retained profits.

Further reading: My BVXP Buy report | All my BVXP posts | BVXP website

Results summary

Revenue, profit and dividend

- Although the preceding H1 supplied a positive outlook…

[H1 2024] “In conclusion, our core business has performed in line with expectations with growth in China being a key feature. Troponin revenues did not accelerate quite as expected but we continue to believe that the headwinds are temporary and operational in nature. We remain excited as the scientific output of our Gothenburg Alzheimer’s collaboration slowly translates into commercial potential. We look forward to further progress in the second half of the year and beyond.”

- …this FY was below BVXP’s expectations.

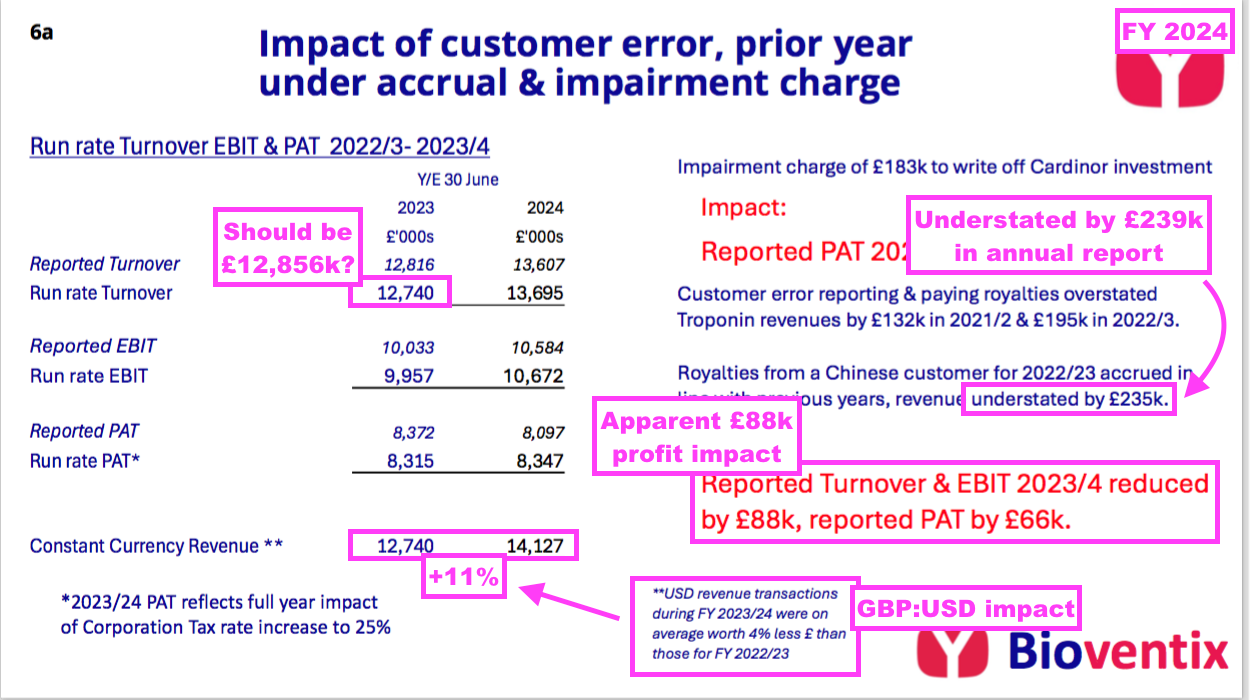

- The disappointment followed a “customer error in the incorrect application of a historic royalty percentage“, which led BVXP to admit royalties from its troponin antibody had been “overreported and overpaid” since FY 2022 (see Troponin).

- To correct the accounts for the error, the £327k of “overreported and overpaid” troponin revenue previously recognised during FYs 2022 and 2023 was subtracted from this FY’s revenue.

- This FY’s royalty error emphasised BVXP’s:

- Dependency on accurate customer calculations in order to publish reliable financial information, and;

- Lack of ‘visibility’ over the ‘downstream’ usage of its antibodies (see Royalty income and physical sales).

- A further FY complication was the delayed revenue recognition of £235k from a Chinese customer, which had in fact been earned during the comparable FY (see Royalty income and physical sales).

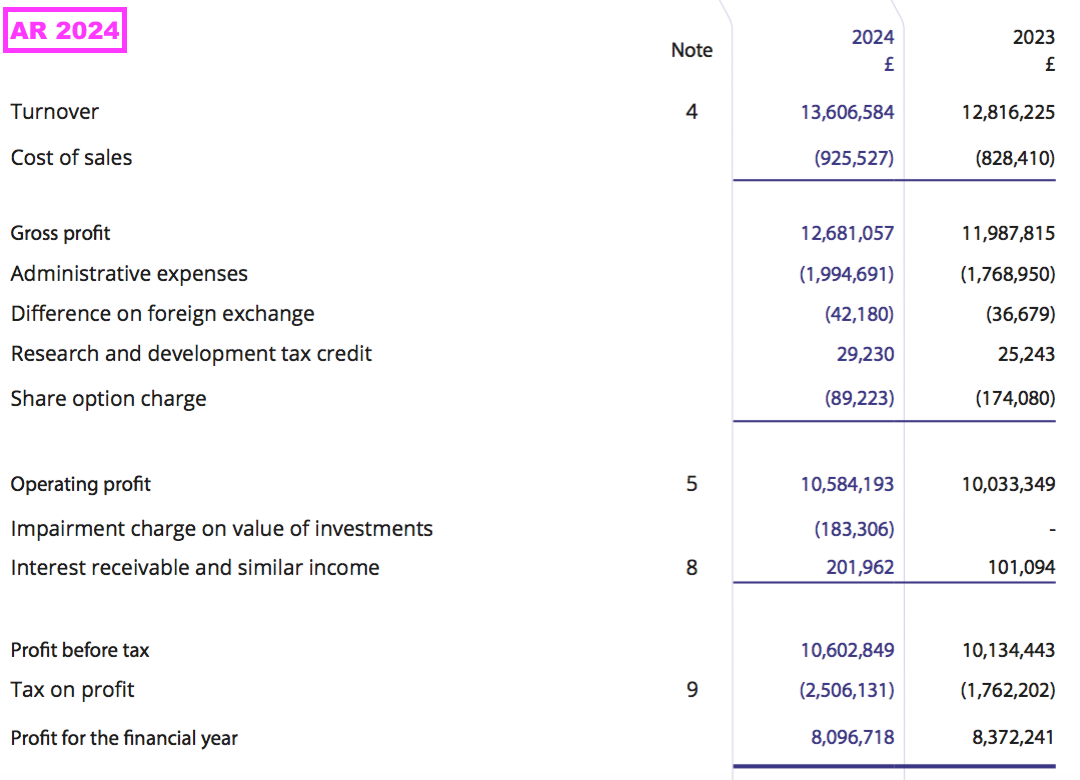

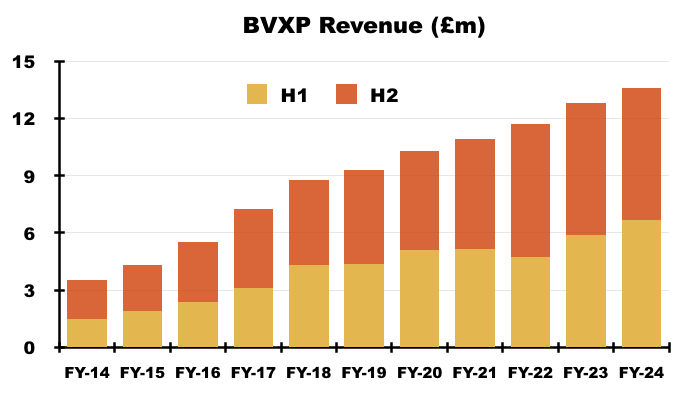

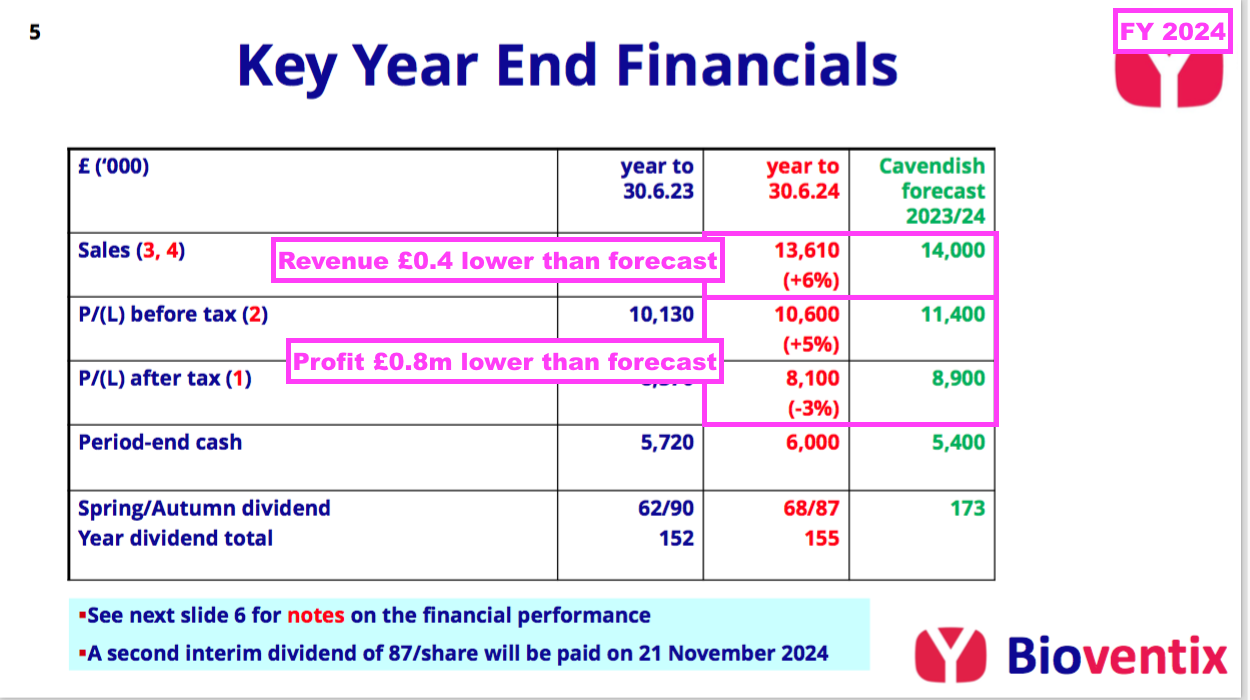

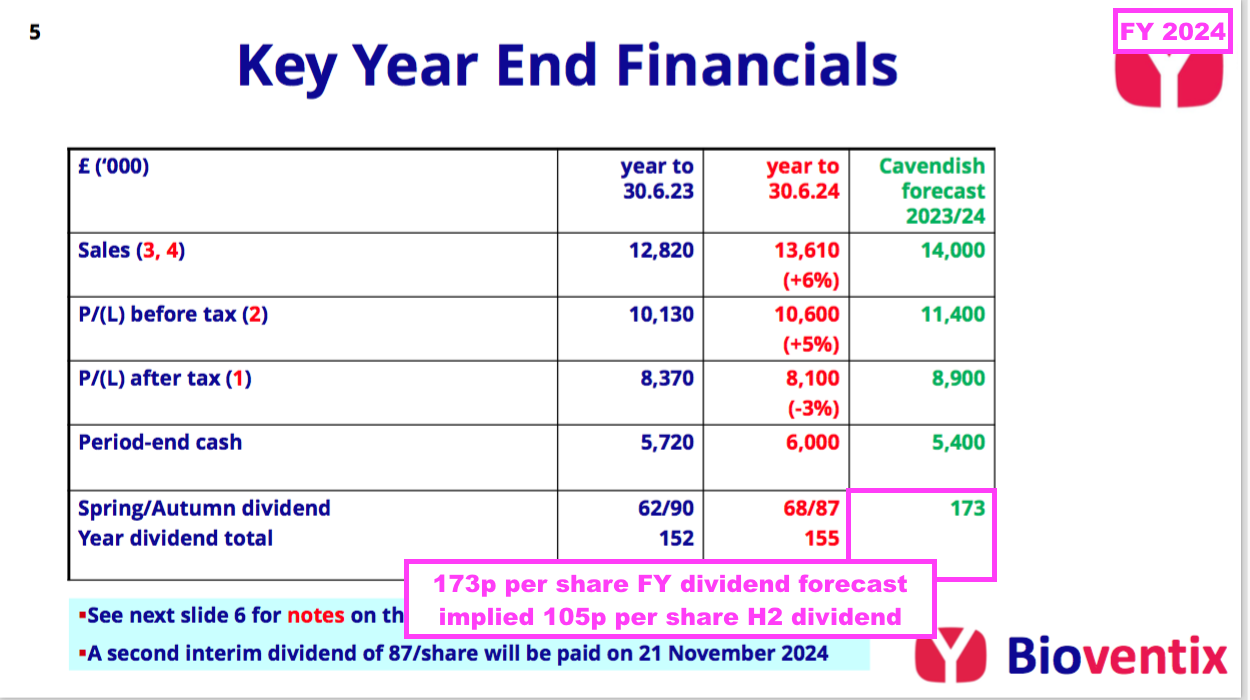

- Statutory revenue for this FY — which includes the £327k troponin subtraction and the delayed £235k Chinese income — gained 6% to £13.6m to set a new FY record:

- Mind you, BVXP’s house broker had expected £14.0m:

- After H1 revenue gained 13%, this FY indicated statutory H2 revenue was flat at £6.9m.

- Adjusting for the troponin error and delayed Chinese income, BVXP claimed this FY’s “run-rate” revenue advanced 7% from £12.7m to £13.7m:

- Note that BVXP’s “run-rate” revenue for the comparable FY is shown as £12,740k, but might actually be £12,856k (i.e. the £12,816k reported originally less that year’s £195k incorrect troponin revenue plus the £235k delayed Chinese income).

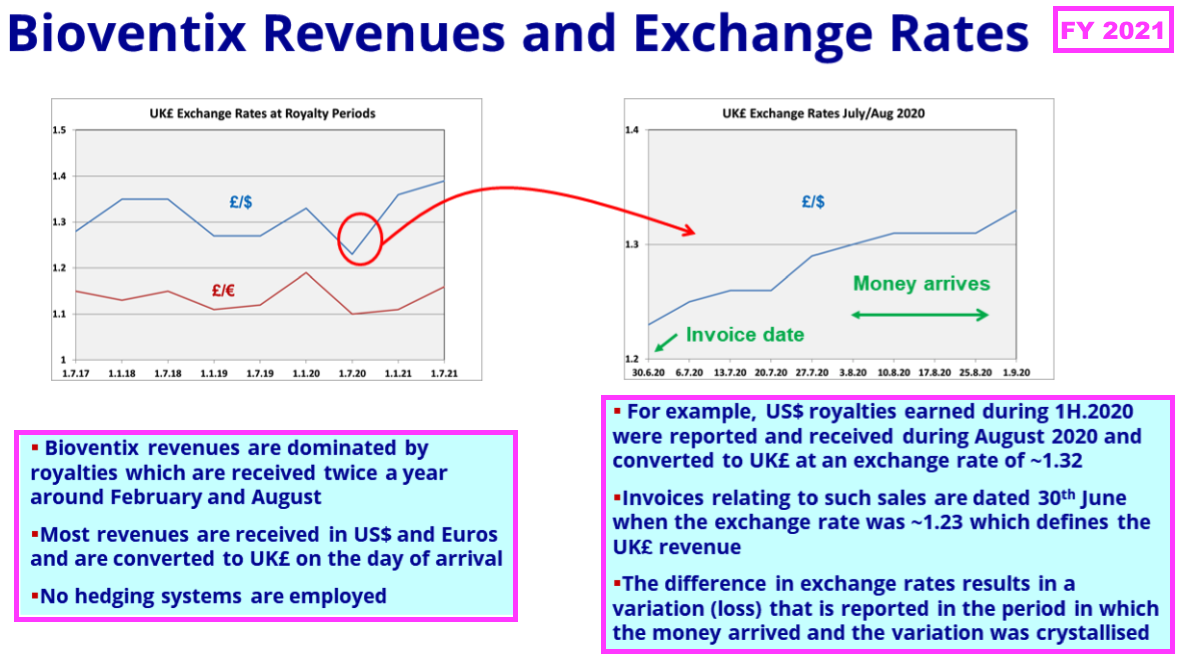

- This FY complicated the top-line performance further by highlighting the impact of exchange rates, with FY constant-currency “run-rate” revenue apparently up 11% to £14.1m.

- This FY reiterated at least 50% of revenue is earned in USD…

“We estimate that 50-60% of our total sales are directly linked to US Dollars via physical product pricing in US Dollars or indirectly linked to US Dollars via royalties based on downstream US Dollar sales. The remainder of the currency split is dominated by Euros and important Asian currencies”

- …while FY 2021 explained how royalty revenue in particular is influenced by exchange rates prevailing on the date of the each balance sheet:

- Royalty invoices for the preceding H1 and this FY were dated 31 December 2023 and 30 June 2024, at which point GBP:USD was 1.275 and 1.265

- Royalty invoices for the comparable H1 and comparable FY were dated 31 December 2022 and 30 June 2023, at which point GBP:USD was 1.209 and 1.270.

- As such, USD-invoiced royalty revenue appeared to be translated into GBP at an average 3% lower rate during this FY versus the comparable FY.

- BVXP said the troponin- and Chinese-revenue rejigs had a minimal £88k effect on operating profit.

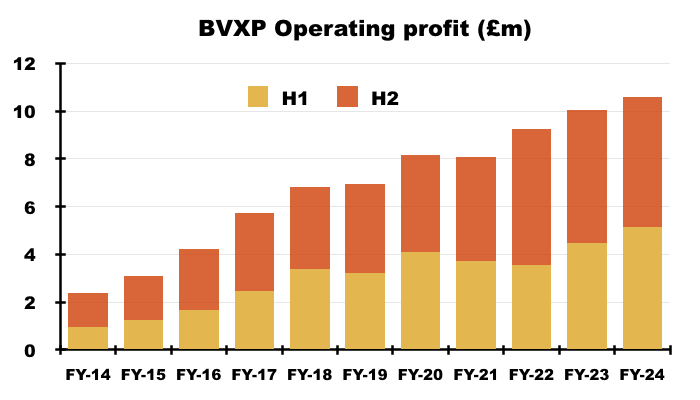

- Statutory FY operating profit gained 5% to £10.6m to set a new FY record:

- But statutory H2 operating profit did slip 2% to £5.4m.

- This FY included BVXP’s first ‘exceptional’ item since FY 2014: an £183k write-down of the CardiNor investment (see Other R&D).

- While the troponin miscalculation, delayed Chinese revenue and CardiNor write-down may seem minor niggles given this FY’s statutory profit topped £10m, a lower-than-expected H2 dividend illustrated this FY’s under-performance.

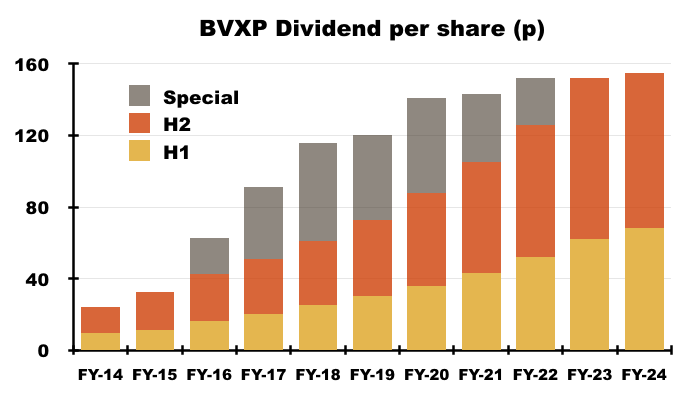

- The preceding H1 showed BVXP’s house broker projecting a 173p per share FY dividend that implied a potential 105p per share dividend for H2:

- However, this FY declared an 87p per share H2 dividend — 18p per share lower than the house broker’s 105p per share forecast and 3p per share lower than the comparable H2 2023 payout:

- This FY referred to an “established dividend policy“:

“In consideration of our established dividend policy and the available cash flows, the Board is pleased to announce a second interim dividend of 87 pence per share which, when added to the first interim dividend of 68 pence per share makes a total of 155 pence per share for the current year”

- The preceding H1 confirmed the “established dividend policy” expected future payouts would advance in tandem with earnings:

[H1 2024] “Recent changes to the headline rate of Corporation Tax has had an impact on our reported earnings and cash flows. Nevertheless, we will endeavour to follow our established dividend policy of increasing our distributions to shareholders in line with increases in our post tax profit.”

- Sure enough, H2 earnings (excluding the CardiNor write-off and associated tax) were approximately £4.2m — roughly 3% lower than the comparable H2 earnings of £4.4m to match the 3% reduction to the H2 dividend.

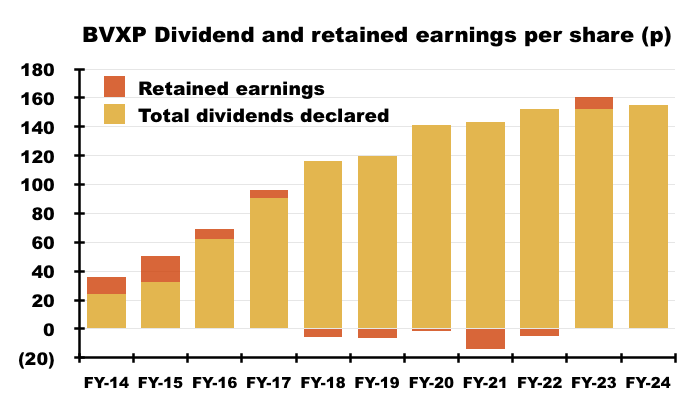

- Despite the lower H2 payout, the 10% lift to the preceding H1 dividend ensured the FY dividend was 155p per share — up 3p per share on the comparable FY and a new FY payout record.

- The 3p per share reduction to the H2 dividend equates to approximately £157k, and compares to the £327k overstated troponin revenue and delayed £235k Chinese income.

- The 3p per share reduction to the H2 dividend was BVXP’s first lower payout for either H1 or H2 since the FY 2010 flotation.

Royalty income and physical sales

- BVXP’s customers are predominantly major in vitro diagnostic (IVD) companies, such as Roche, Siemens and Abbott, which manufacture blood-testing machines and incorporate BVXP’s antibodies into blood-test reagent packs to help diagnose a variety of health conditions:

- BVXP’s revenue is earned mostly through IVD customers:

- Purchasing BVXP’s antibodies and incorporating them into reagent packs, and;

- Paying a small royalty for every reagent pack subsequently sold ‘downstream’ to the owners of the blood-test machines (typically hospitals).

- The amounts collected through physical sales and royalties is determined mostly by the volume of antibodies required for a particular blood test. Some tests require 100s or 1000s more antibodies than others:

- Antibodies used in large volumes tend to earn larger physical sales and collect smaller royalties, whereas antibodies used in smaller volumes tend to earn smaller physical sales but collect larger royalties.

- BVXP’s revenue has historically been split approximately two-thirds royalties and one-third physical sales:

- Both revenue sources have expanded at similar rates:

- During this FY, royalty income advanced by 7% (to £9.1m) while physical sales advanced by 5% (to £4.5m), and;

- Between FY 2019 and this FY, royalty income advanced by 46% while physical sales advanced by 48%.

- BVXP’s royalties typically capture approximately 2% of the ‘downstream’ sales of the blood-test regent packs that incorporate the company’s antibodies.

- This FY included a revamped section about royalty-income risk:

“The Company’s key income stream is that of royalties; a contractual obligation due by the customer to Bioventix plc, the value of which is determined as a percentage of the sales values generated over a defined period by those customers from their products that utilise antibodies created by Bioventix plc.

Royalty rates are set at the start of the royalty agreement with each customer and any exposure to sales price risk is linked solely to the revenues generated by the Company’s customers.”

- While BVXP’s royalty percentage is fixed, the associated reagent-pack sales to which the royalty percentage is applied can vary… meaning BVXP is not entirely in control of its eventual royalty income.

- Board remarks at the 2022 AGM confirmed BVXP’s “limited visibility” over its royalty income. Attendees were told:

- BXVP does not know what its customers charge for blood-test reagent packs, and if/when those charges increase or decrease.

- Similarly, BVXP does not know the volume of reagent packs sold by its customers that include royalty-earning antibodies;

- BVXP therefore has “limited visibility” to analyse its royalty income, and;

- “The royalty is based on net sales after deductions and that is all [the customers] are required to declare.”

- The aforementioned “overreported and overpaid” troponin revenue prompted this FY to include a new risk warning about royalty calculations:

“The value of royalties due is calculated, declared and paid by customers. The receipt of funds by Bioventix plc, in respect of royalties, is taken as strong evidence that such revenue is due and has been correctly recorded and Bioventix plc is reliant upon the accuracy of customer’s calculations in its reporting of royalty revenue and the correct recognition of such revenue both in terms of its value and its timing. There is a risk, should customers make errors in the calculation and payment of royalties, that such revenue may be misstated in the financial statements either in the timing of revenue recognition or of the quantum of such revenue.”

- This FY registered BVXP’s third customer-royalty miscalculation. The previous two errors were fortunately underpayments and were described by BVXP as “back-dated” royalties:

[H1 2018] “During the half-year, an internal audit at one of our customers identified a back-dated royalty stream of £0.77 million that was due from 1 July 2014 to 30 June 2017 and therefore outside the current reporting period. We have therefore identified these back-royalties separately in the accounts.

[FY 2014] “There is an exceptional revenue item of £190k, which resulted from an internal audit at one of out licensees that revealed a profit code on which back-dated royalties were owed for preceding years“

- The comparable FY revealed China accounted for approximately half of all physical sales:

[FY 2023] “Sales to China remain strong accounting for ~50% of total physical sales. Chinese downstream assay price pressure has increased through aggressive central health authority procurement mechanisms”

- This FY suggested China continued to account for half of all physical sales, and confirmed “more significant” Chinese royalties should soon be collected:

“Our shipments of physical antibody to China continued to increase. Some sales are made directly and some are made through five appointed distributors. More regulatory approvals for domestic Chinese customers using our antibodies have been registered, leading to more significant flows of royalty payments owing from these customers.“

- Sales to China have grown significantly over time. FY 2013 reported China represented approximately 10% of all shipments:

[FY 2013] “We are also cautiously optimistic about growth prospects in China. There are rapidly emerging Chinese customers and this represents a growth opportunity. It is noteworthy that in the financial year, around 10% of Bioventix shipments (including samples) were destined for China. The actual revenues are less than 10% of the total but the volume of shipments is encouraging for future growth.”

- This FY acknowledged how Chinese customers may pay their royalties a year after utilising BVXP’s antibodies:

“Chinese customers declare and pay royalties in arrears on a calendar year basis and we therefore have to accrue for such revenue, in both full year and interim results, basing our revenue expectation on previous experience. As a result of internal and external audit processes, it was only in May 2024 that we received payment from a Chinese customer for the royalties earned in 2023 and therefore our revenue for 2023/24 has benefited by £239k from our prudent assessment of accrued royalty revenue in respect of previous periods.”

- In contrast, BVXP’s established EU/US customers typically pay their royalties:

- During August for BVXP antibodies utilised between January and June, and;

- During February for BVXP antibodies utilised between July and December.

- This FY reiterated China’s positive short-term prospects and longer-term “technology development” threat:

“The prospects for further short term growth in China are good. Longer term, price pressures and continued antibody technology development in China constitute an anticipated threat. In addition to this, the current global geopolitical climate has stimulated the desire for “on-shoring” supply chains and our Chinese customers are likely to be influenced by this trend.”

- Board remarks at the 2024 AGM provided further details of Chinese IVD companies. Attendees were told:

- The likes of Mindray, Snibe and Autobio are “modelling themselves very aggressively” on EU/US IVD equivalents;

- BVXP’s Chinese agreements are now focused on a handful of local operators that the company knows “very, very well“;

- Sales are no longer made to Chinese academics/distributors;

- Chinese competition is “very serious” and “we’re stuck with that“;

- Chinese IVD companies appear to be focusing more on new tests rather than revamping old tests, and;

- Switching from a BVXP antibody to a Chinese antibody would be as “non-trivial” for a Chinese IVD company as it would be for a EU/US IVD company.

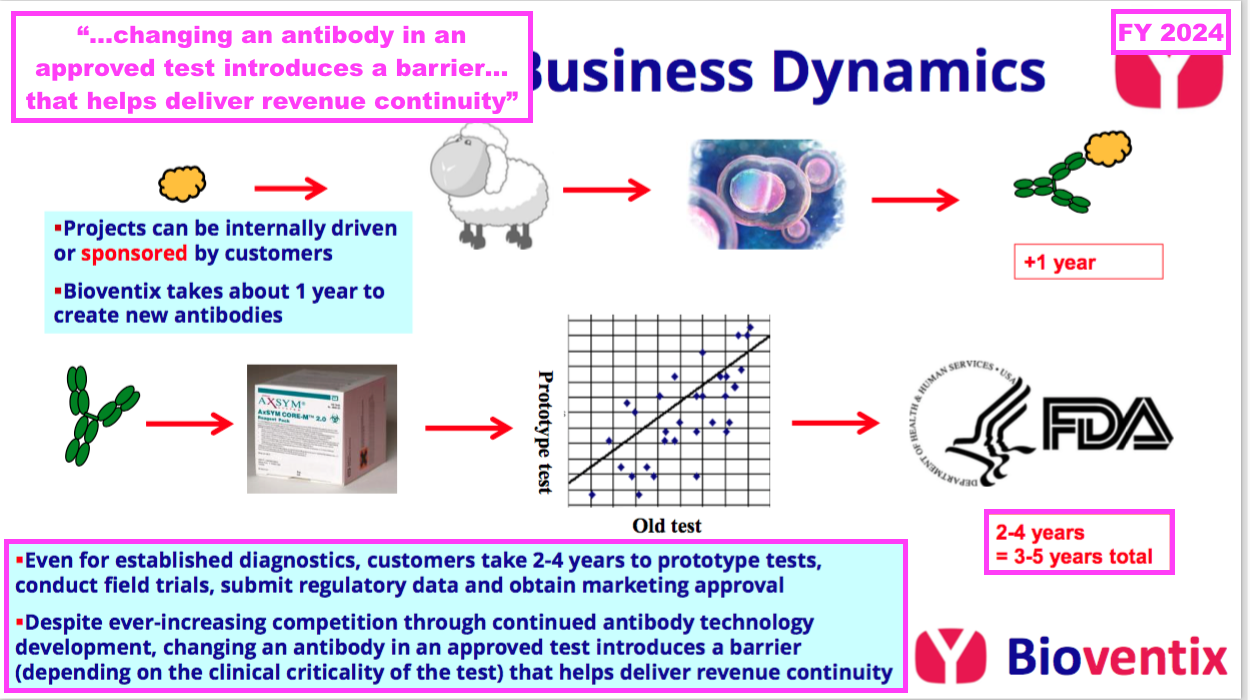

- This FY reiterated why substituting proven diagnostic antibodies is “non trivial“: the replacement version must undertake clinical tests and obtain regulatory approval before a commercial launch:

“The process of subsequent development thereafter by our customers can take many years before registration or approval from the relevant authority… is obtained and products can be sold to the benefit of the customers, and of course Bioventix, through the agreed sales royalty.

However, because of the resource required to gain such approvals, after having achieved approval for an accurate diagnostic test using a Bioventix antibody, there is a natural incentive for continued antibody use. This results in a barrier to entry for potential replacement antibodies which would require at least partial repetition of the approval process arising on a change from one antibody to another.

This barrier to antibody replacement arises from a combination of factors driven by the clinical criticality of the test and the potential consequences of making such a change, which include the time and cost to register any changes required to validate the performance of the replacement antibody.“

- As such, the healthcare/IVD industry can be very reluctant to replace a proven blood test, which means established diagnostic antibodies can remain commercial for extended periods.

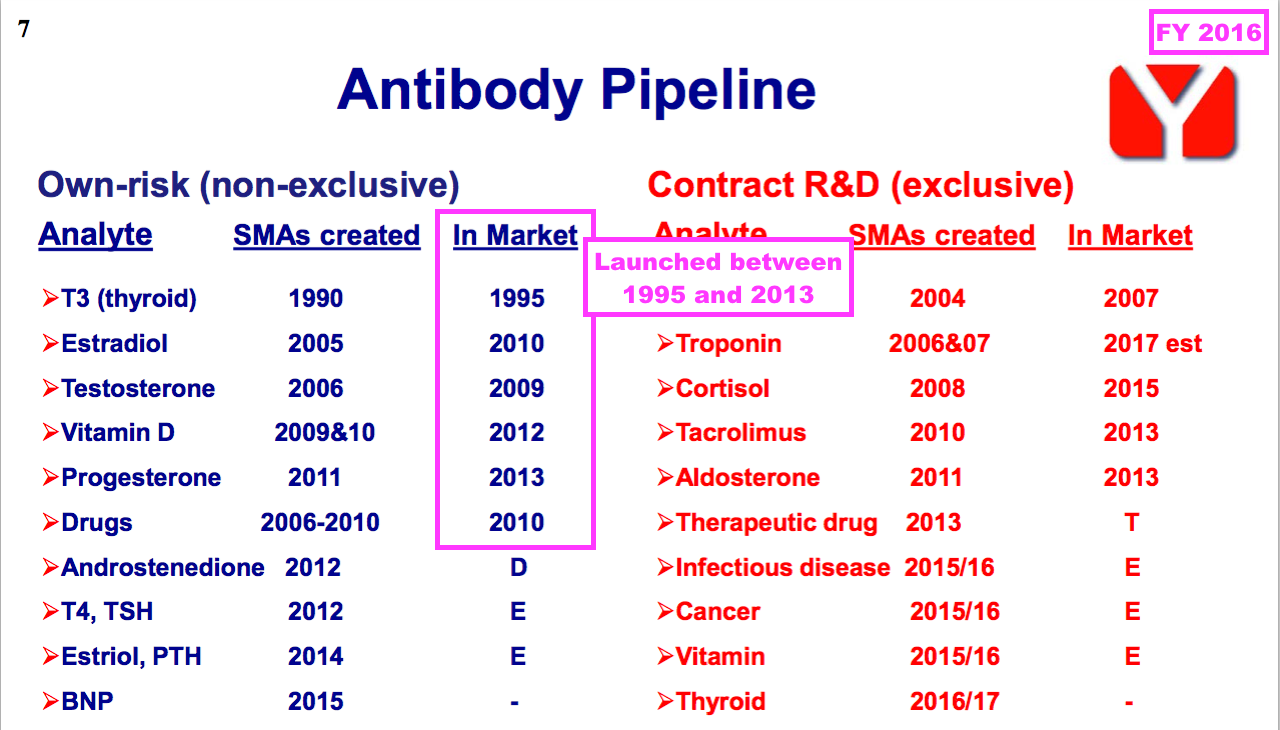

- FY 2016 revealed how a number of BVXP’s current antibodies were first launched more than ten years ago, with Tri-iodothyroxine (T3) seemingly celebrating an astounding 30 years on the market (see Other core antibodies):

- This FY’s disappointing troponin progress could be evidence that upgraded antibodies offering significant diagnostic enhancements may not always be able to dislodge an incumbent as much as expected (see Troponin).

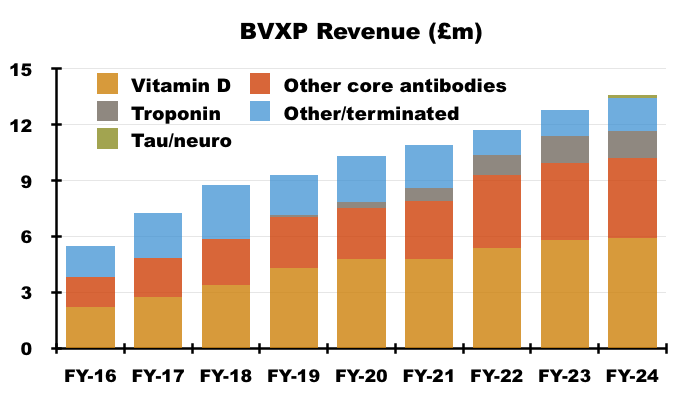

Vitamin D

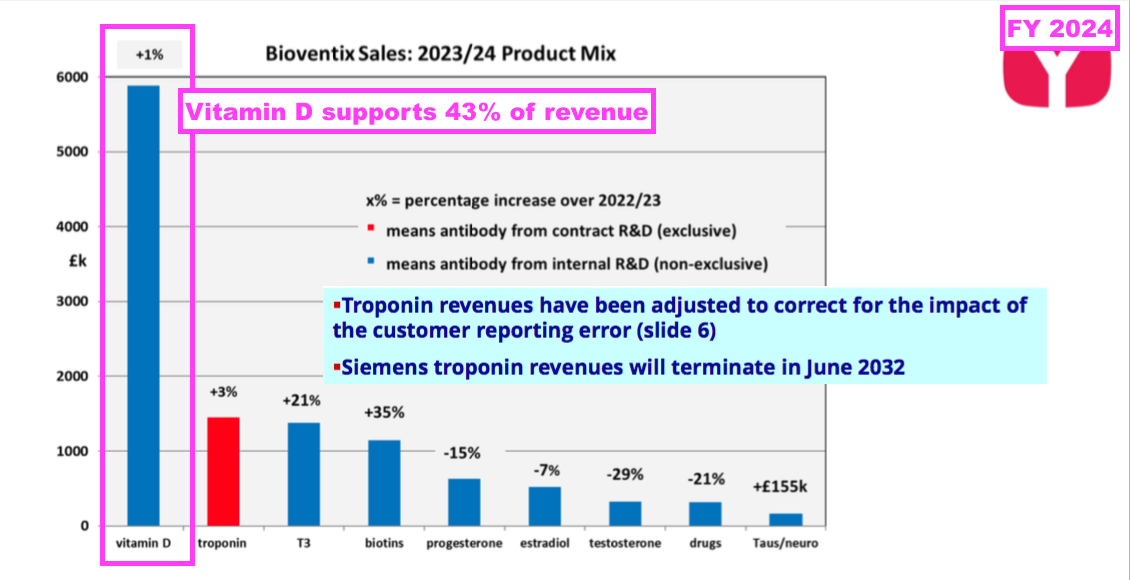

- BVXP’s vitamin D antibody remains by far the company’s best seller, and during this FY increased its revenue by 1% to reflect a “relatively mature global IVD market”:

“Our most significant revenue stream continues to come from the vitamin D antibody called vitD3.5H10. This antibody is used by a significant number of diagnostic companies around the world for use in vitamin D deficiency testing. Sales of vitD3.5H10 increased by 1% to £5.9 million which reflects analysts’ expectation for a relatively mature global IVD market.“

- The comparable FY revealed vitamin D revenue gained 7%, which also reflected a “relatively mature global IVD market”:

[FY 2023] “Our most significant revenue stream continues to come from the vitamin D antibody called vitD3.5H10. This antibody is used by a number of small, medium and large diagnostic companies around the world for use in vitamin D deficiency testing. Sales of vitD3.5H10 increased by 7% to £5.8 million which reflects analysts’ expectation for a relatively mature global IVD market.”

- Vitamin D represented 43% of total FY revenue:

- Vitamin D has represented between 38% of revenue (FY 2017) and 47% of revenue (FY 2020) since FY 2016:

- BVXP began claiming during FY 2017 that vitamin D sales would “plateau” and three years ago talked of “price erosion in downstream markets“:

[H1 2022] “As reported previously, the growth rates for our vitamin D antibody sales were not expected to match those seen in recent financial years and a plateau in the downstream global vitamin D assay market had been anticipated. Sales associated with assay formats using larger quantities of antibody per test suffered more as price erosion in downstream markets puts pressure on costly “antibody-hungry” products“.

- Maybe this FY’s 1% advance is confirmation vitamin D revenue has finally reached a ‘plateau’.

- Board remarks at the 2022 AGM claimed the vitamin D “price erosion” had been experienced for some years and was triggered by large IVD companies introducing new tests.

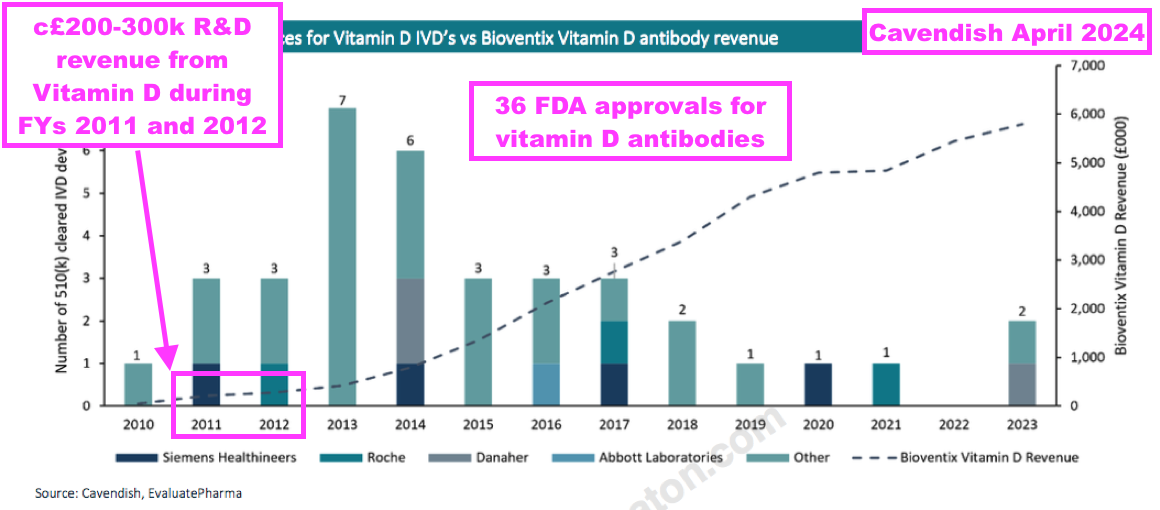

- An informative broker note issued last year highlighted 36 vitamin D tests being approved for use within the United States between 2010 and 2023:

- BVXP started development on vitamin D during 2008 and revenue was first acheived during 2011.

- Note that vitamin D “moved into large-scale manufacturing” and generated R&D-revenue (from customers only testing the antibody) during FYs 2011 and 2012 — i.e. before a wider commercial test was launched:

[FY 2011] “One of the most exciting developments for the company has been the vitamin D project which has been the subject of intensive internal R&D since the summer of 2008. A leading antibody called vitD3.5H10 has moved into large-scale manufacturing at the company in order to supply increased quantities of antibody required for our customers’ own R&D use. Revenue from the supply of this product has been generated for the first time during the period. No major licensing deals have yet been concluded, however, the Directors are optimistic about the future value of this particular antibody and anticipate that significant licensing deals will be forthcoming in the future.“

[FY 2012] “During the year Bioventix’s leading vitamin D antibody, vitD3.5H10, moved into large-scale manufacture in response to customer demand and revenue from the supply of this product has continued to grow during the period. Whilst no significant commercial vitamin D assays based on vitD3.5H10 are currently in the market, the Directors remain optimistic that this antibody will generate revenues for the Company in future periods. The Company has also entered into additional licensing deals with major diagnostics companies in respect of vitD3.5H10.”

- From that broker note above, vitamin D appeared to generate R&D-revenue of approximately £200k during FY 2011 and approximately £300k during FY 2012.

- Vitamin D generating R&D-revenue may have positive omens for BVXP’s Alzheimer’s antibodies, three of which have recently moved into “large-scale production for commercial supply” and started to earn R&D-revenue from customer testing (see Alzheimer’s R&D: revenue).

- Vitamin D revenue going from zero to almost £6m within 13 years may give some idea as to the potential of BVXP’s Alzheimer’s antibodies (see Alzheimer’s R&D: revenue and Valuation)

Troponin

- The preceding H1 acknowledged revenue from troponin antibodies — used within blood tests to help diagnose suspected heart attacks — had been “a little below expectation“:

[H1 2024] “Whilst our total sales continue to grow, our sales relating to troponin antibodies were a little below expectation.

- At the time BVXP cited “temporary operational issues” at its customers:

[H1 2024] “We continue to believe that temporary operational issues experienced by our partner customers have slowed the rollout of their improved troponin assays. Whilst this has inhibited growth short term, there is no obvious reason to doubt the previous forecasts for future growth of troponin related revenues in the longer term.”

- This FY then admitted troponin revenue had been “overreported and overpaid” during FYs 2022 and 2023 by a total £327k:

“During the year the Company became aware that, due to a customer error in the incorrect application of a historic royalty percentage, they had overreported and overpaid troponin royalty revenues since July 2021. Royalty revenues for the financial years 2021/22 and 2022/23 were overstated by £132k and £195k respectively. These amounts are immaterial in respect of each of the affected periods and therefore the Company is not required to restate the audited financial statements for those years; however, the cumulative effect of a reduction of £327k in respect of such royalty revenue has been included in the financial statements for the current year to 30 June 2024.”

- This troponin error emphasised BVXP’s aforementioned “limited visibility” towards customer royalty payments.

- With hindsight, BVXP clearly had no inkling a customer was calculating troponin royalties incorrectly…

- …and may have been simply guessing slower troponin revenue was due to the customer experiencing “temporary operational issues“.

- Troponin revenue for FY 2022 was originally reported as £1,230k, but following the recalculation was in fact £1,098k — i.e. a 12% overstatement.

- Troponin revenue for FY 2023 was originally reported as £1,610k, but following the recalculation was in fact £1,415k — i.e. a 14% overstatement.

- This FY revealed (correctly calculated) troponin revenue gained 3% to £1.45m and was “below… expectations”:

“After correctly allocating the revenue to each of the years 2023/24 and 2022/23, our total troponin antibody royalty revenue from Siemens Healthineers and another separate technology sub-license increased by 3% during the year from £1.41 million to £1.45 million. The level of these royalties and their growth are below our previous expectations based on downstream assumptions.”

- Board remarks at the 2024 AGM provided further troponin commentary. Attendees were told:

- The royalty error was “genuinely disappointing“;

- Management was “perhaps a little bit overly optimistic” about troponin’s inherent prospects, and;

- Revenue from troponin’s current application — diagnosing heart attacks within A&E departments — was now “mature“.

- Such “mature” troponin revenue supported 11% of this FY’s total top line.

- Perhaps troponin was never destined to meet BVXP’s expectations.

- With hindsight, the early signs were not promising when, a few months after troponin’s commercial launch during 2017, BVXP talked of an “education period” that had slowed the antibody’s initial adoption:

[H1 2018] “We reported in May that our troponin (heart attack diagnostic) partner, Siemens Healthineers, released a new test outside the US market that helps facilitate a faster diagnosis of patients presenting with chest pain in an A&E setting. The rate at which this new test will be adopted by Siemens customers in hospitals in the EU, Asia and elsewhere outside the US is unfortunately not something of which we have detailed knowledge.

Whilst it is clear that a quicker test will be of benefit to patients, clinicians and hospital budget holders, it is also clear that there is likely to be an education period during which clinicians become comfortable with a significant change in diagnostic practices that can result in non-MI (i.e. patients not having a heart attack) being released from A&E much earlier. We will develop a better understanding of this matter during 2018.”

- FY 2018 then confirmed the initial troponin revenue was below expectations:

[FY 2018] “We have reported previously on the importance of our troponin project with Siemens Healthineers. Sales during the reporting period were not significant and below our expectation. We have no reason to question our belief that this project will generate significant value into the future and Siemens recent US approval from the FDA should help in this regard.“

- The “education period” that slowed troponin’s initial adoption may now suggest BVXP’s ‘downstream’ customers were at the time quite happy with their existing blood tests for diagnosing suspected heart attacks.

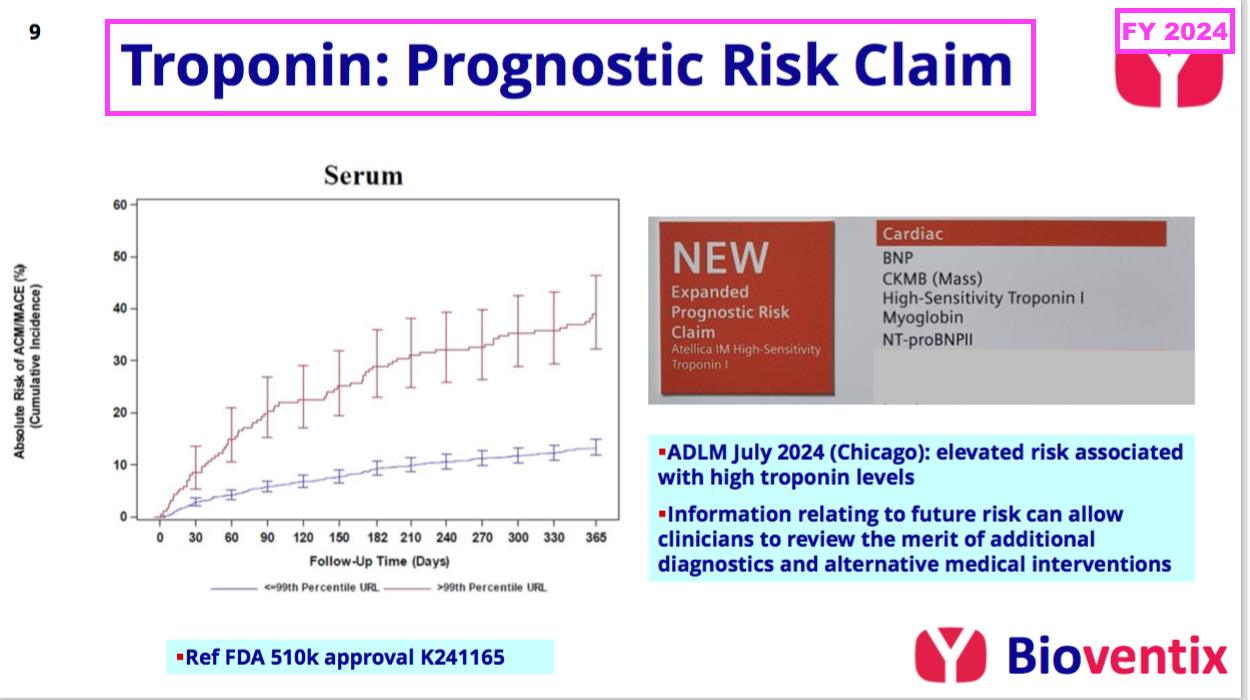

- This FY revealed BVXP’s troponin revenue could be enhanced by the same blood test being used to “assess the impending risk of a future adverse cardiac event“:

“In contrast to the disappointment of troponin sales in the current application of acute chest pain (i.e. suspected heart attack in A&E centres), we are pleased to note that Siemens have received FDA approval for a revised label claim for their troponin assay that covers a new prognostic application. This enables troponin levels to be measured in “at risk” patients and/or patients who have already been diagnosed with a cardiac condition, whose troponin levels may now be measured to assess their impending risk of a future adverse cardiac event.

This risk information can then be used to help clinicians consider additional diagnostic procedures or to review therapeutic alternatives. We expect that this new application will stimulate additional troponin assay use and our associated royalties, thus increasing the market opportunity.”

- Board remarks at the 2024 AGM provided further details of the secondary troponin test. Attendees were told:

- Siemens is “optimistic” this “whole new market for troponin” will “boost sales“;

- Some cardiologists will now “just measure everybody” who visits their clinics with this secondary test, and;

- The first indication of progress should have emerged by March 2025.

- Note that troponin revenue is generated through Siemens and a separate sub-licensee:

“Our total troponin antibody royalty revenue from Siemens Healthineers and another separate technology sub-license increased by 3% during the year from £1.41 million to £1.45 million.”

- FY 2018 implied the sub-licensee was Beckman Coulter:

[FY 2018] “One of Siemens competitors, Beckman Coulter, also offers a new high sensitivity troponin assay. It is known through access to FDA data that this new assay also features a sheep monoclonal antibody. In accordance with our historic exclusivity agreement with Siemens (which we negotiated with Dade Behring, a company later acquired by Siemens) we have played no part in the development of this antibody. Nevertheless, the means by which the antibody was created by another Bioventix licensee does leave us in a position whereby this product will generate some revenue for the company in the future.“

- This FY reiterated troponin revenue from Siemens will stop during 2032:

“As previously disclosed, Siemens troponin revenues will terminate for contractual reasons in June 2032.”

- The wording seemingly allows BVXP to collect troponin revenue from Beckman Coulter beyond 2032.

- Siemens funded BVXP’s troponin R&D and has always been BVXP’s primary source of troponin revenue. I presume the royalty error occurred at Siemens and not Beckman Coulter.

Other core antibodies

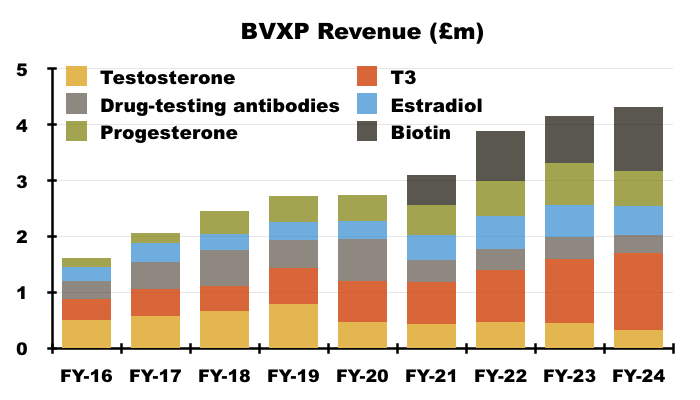

- BVXP’s “other core historic” antibodies experienced a mixed FY:

• T3 (tri-iodothyronine): £1.38 million (+21%)

• Biotins and biotin blockers: £1.14 million (+35%);

• Progesterone: £0.63 million (-15%)

• Estradiol: £0.52 million (-7%)

• Testosterone: £0.33 million (-29%)

• Drug-testing antibodies: £0.32 million (-21%).

- Revenue from these other core antibodies collectively gained 4% to £4.3m, although only T3 and biotin made positive progress.

- Despite T3 being on the market for 30 years, its revenue gained 21% during this FY and has ballooned 261% since FY 2016:

- I understand biotin has been on the market since 1999 (2022 AGM), and during this FY its revenue increased 35%. Biotin revenue was first disclosed during FY 2022 (up +67% to £900k), and has now more than doubled since FY 2021.

- BVXP has never explained why revenue from T3 and biotin have increased so significantly…

- …which is no doubt due to BVXP’s aforementioned “limited visibility” towards royalty payments.

- Management comments during this 2016 ShareSoc seminar revealed T3 enjoyed a remarkable 50%-plus global market share.

- I understand biotin revenue may have increased because BVXP’s product could be viewed as an alternative to streptavidin when applying the popular biotin-streptavidin pairing within blood-testing chemistry (2022 AGM).

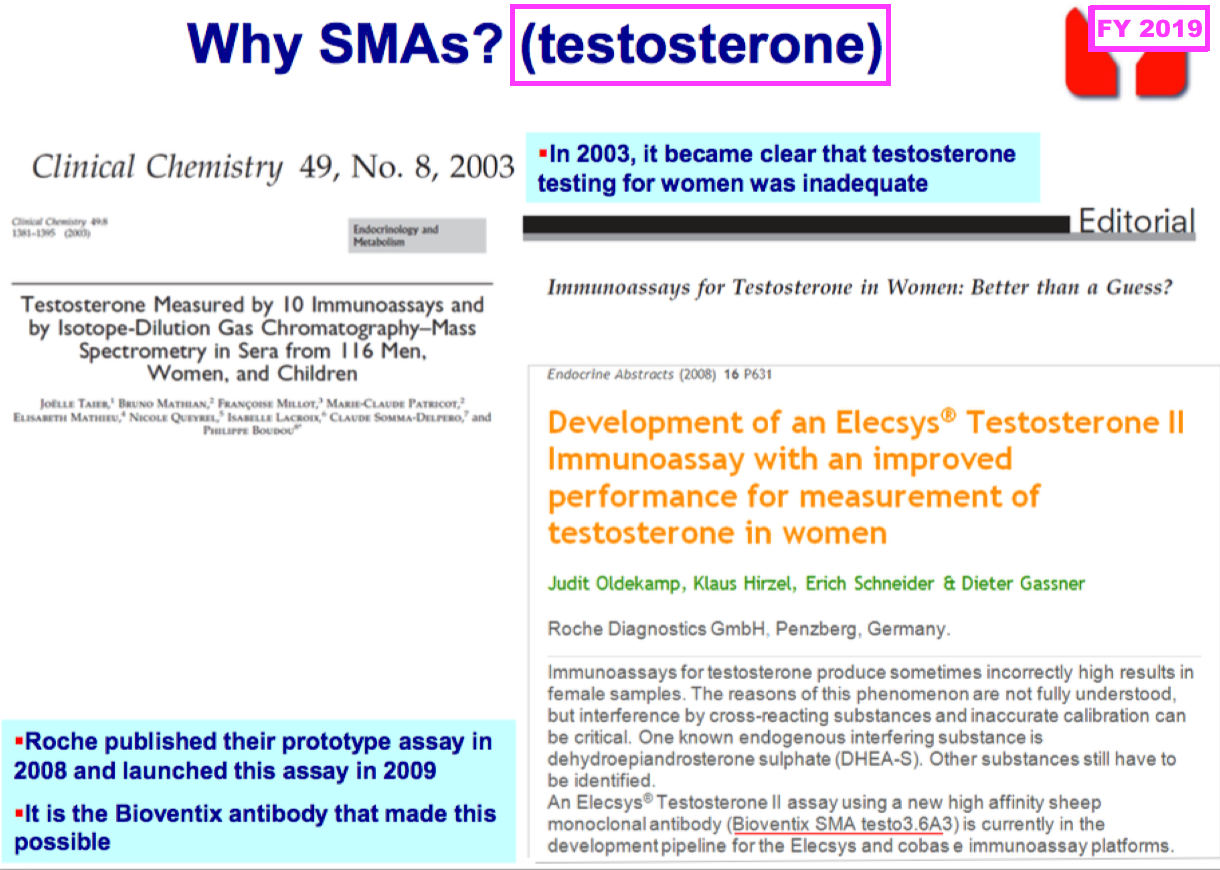

- Among BVXP’s fertility-related products, testosterone revenue has slid an alarming 63% since FY 2019 (from £800k to £330k).

- Testosterone revenue began during 2009 and the test was featured within BVXP’s powerpoints up to FY 2019:

- At launch, BVXP’s testosterone antibody solved a widespread IVD-industry problem of inaccurate blood tests… but the reduced revenue does suggest the IVD industry has now found at least one alternative supplier.

- Since FY 2017, revenue from progesterone has almost tripled (to £630k) while revenue from estradiol has doubled (to £520k)… albeit with yearly fluctuations in-between.

- Overall, the other core antibodies (excluding biotin) have collectively almost doubled their revenue to £3.2m since FY 2016, equivalent to a near-9% CAGR.

- But during the five years to this FY, the CAGR reduces to only 3%.

- Management comments during this 2024 ShareSoc seminar suggested the other core antibodies will, collectively, “continue to do well“:

[BVXP seminar 2024] “They all form a portfolio of quite mature antibody products that have been sold for many years and will continue to do well as our business expands, partly in the West, but also in China.”

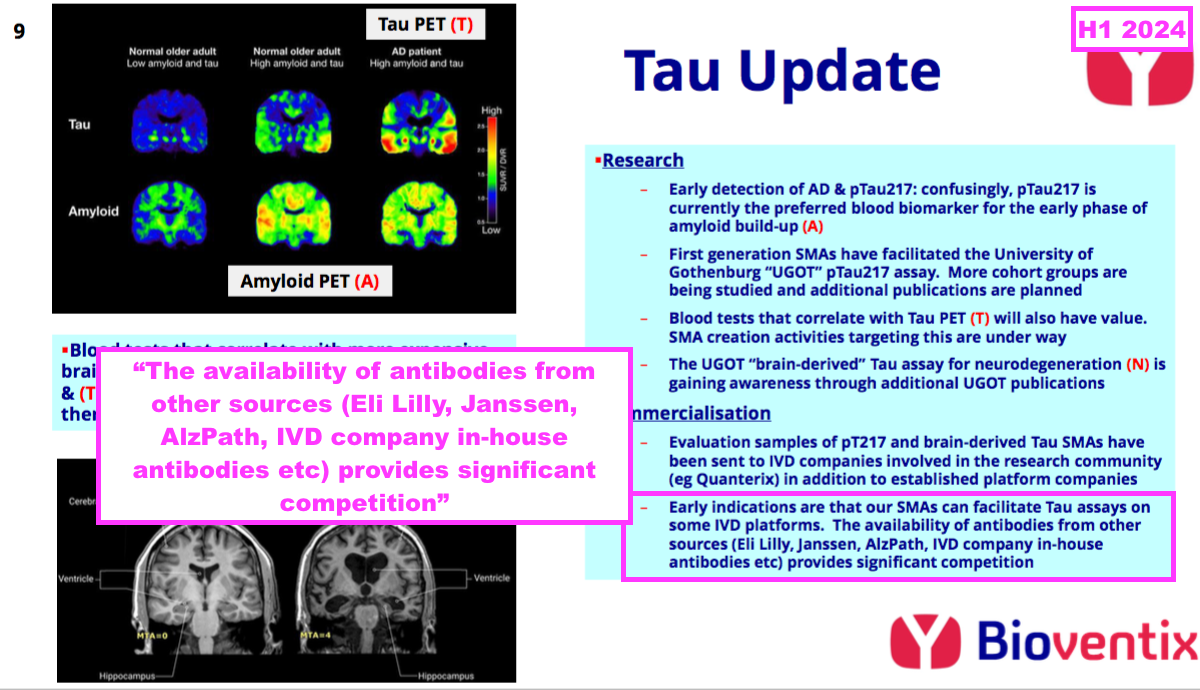

Alzheimer’s R&D: revenue

- By far this FY’s most promising development concerned BVXP’s work creating antibodies to potentially identify and monitor Alzheimer’s disease (AD) through blood tests.

- The AD research achieved FY revenue of £155k:

“Our research into Tau antibodies and Alzheimer’s diagnostics continues to progress and we are delighted that our early work has now translated into a modest revenue stream from antibodies now entering commercial manufacture.

…

Total Tau revenues for the year were above our expectation at £155k.”

- The AD revenue was earned mostly through IVD customers ordering repeat samples for their own R&D:

“Our commercial policy is to supply initial evaluation samples of antibodies free of charge. If antibodies perform well on prototype assay systems at our IVD customers and additional supplies are ordered, these are charged at regular prices and such repeat sales have generated revenues during the year. These revenues are not only additive but also indicate that our antibodies could feature in future commercial assays.”

- This FY suggested the repeat AD orders offered “some encouragement” that BVXP’s AD antibodies will one day feature within mainstream commercial AD blood tests:

“We have supplied a number of major IVD companies with antibodies from our growing Tau antibody portfolio. It is encouraging that a small number of these companies have requested additional quantities of the antibodies supplied. Not only does this add modestly to our overall revenues but it also offers some encouragement that our antibodies will play some part in the future neurological panel offerings of our customers.“

- Management comments during November’s ShareSoc seminar described the rapid emergence of early AD revenue as a “significant observation“:

[BVXP seminar 2024]“And keep in mind, this revenue for tau and neurological products. Now, these are very, very new antibodies that we’ve only just made in the last year or two. So to have quite significant sales of antibodies so quickly, when actually, I’ve just said it takes years before we have any sizeable revenues, is quite a significant observation.”

- Management also claimed during the same seminar that the £155k AD revenue had represented “a lot of antibody“:

[BVXP seminar 2024] “We give little samples free of charge. And if they then want to take their prototypes further, they then have to pay for additional supplies. And £155k is a lot of antibody. So that’s been a very pleasing development as those sales have grown.“

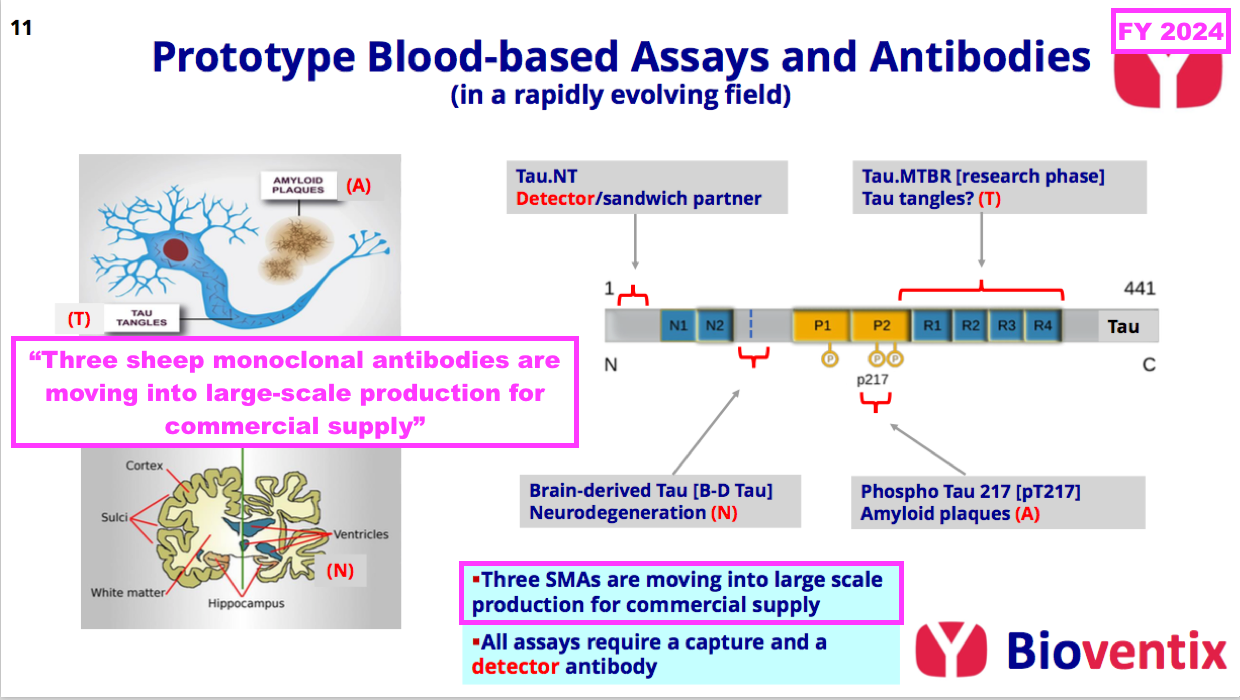

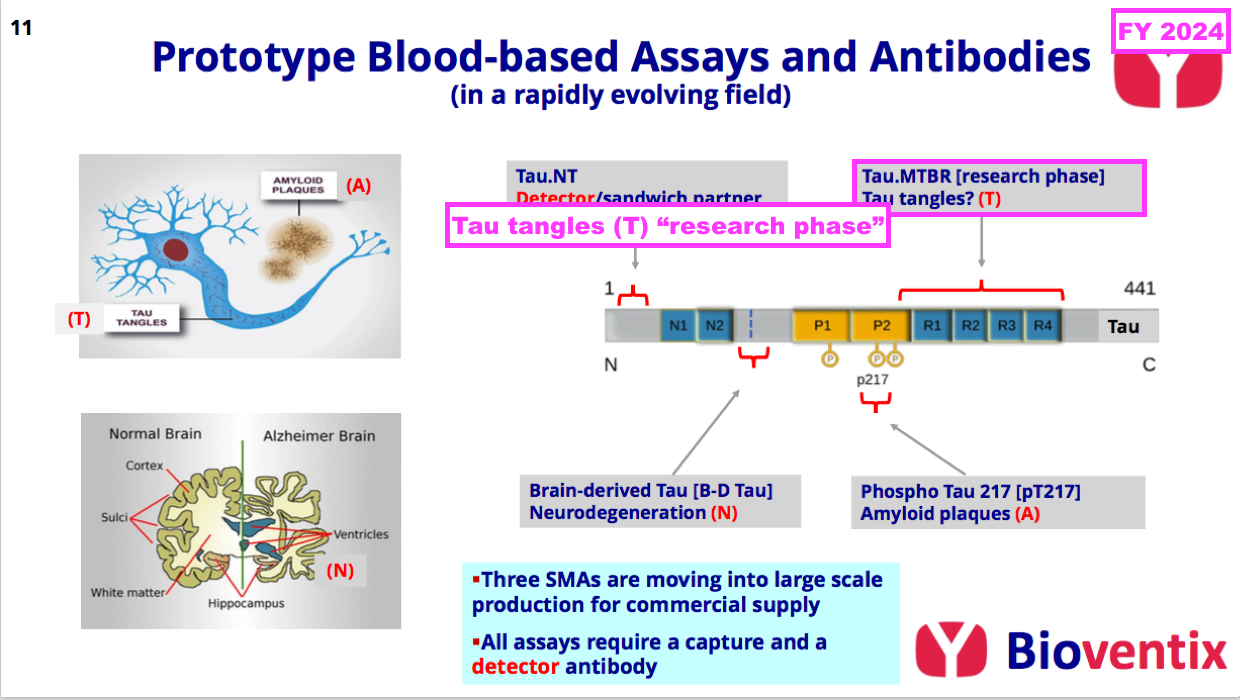

- This FY underlined the promising AD work by announcing the “large-scale production” of three AD antibodies:

- This FY did not reveal exactly which three AD antibodies were moving into “large-scale production“, although by far the most likeliest seems to be TauJ.5H3 brain-derived tau (see Alzheimer’s R&D: neurodegeneration and brain-derived tau).

- Implementing “large-scale production” of AD antibodies for customer R&D purposes is very reminiscent of the aforementioned “large-scale manufacturing” of vitamin D antibodies for customer R&D purposes during FY 2011:

[FY 2011] “One of the most exciting developments for the company has been the vitamin D project which has been the subject of intensive internal R&D since the summer of 2008. A leading antibody called vitD3.5H10 has moved into large scale manufacturing at the company in order to supply increased quantities of antibody required for our customers’ own R&D use.

Revenue from the supply of this product has been generated for the first time during the period. No major licensing deals have yet been concluded, however, the Directors are optimistic about the future value of this particular antibody and anticipate that significant licensing deals will be forthcoming in the future.“

- Vitamin D soon became BVXP’s best seller, which does imply antibodies generating notable income during early R&D testing have quickly proved themselves to be very popular…

- …and should therefore be more likely to become rather lucrative following a full commercial launch.

- This FY’s AD revenue was earned during H2 and board remarks at the 2024 AGM indicated the AD revenue commenced during Q4 (April-June 2024).

- Multiplying the £155k AD revenue by four gives a theoretical £620k annualised AD revenue…

- …which is double the aforementioned £300k or so vitamin D seemingly earned through customer R&D testing during FY 2012.

- Board remarks at the 2024 AGM provided further AD revenue details. Attendees were told:

- By the end of 2025, BVXP ought to know whether its AD antibodies stand any chance of becoming commercial;

- “It’s very important for us to be part of that final selection and that will pretty much cement our position in what we think will be a crucial diagnostic market”;

- NOT to extrapolate the £155k revenue, as the AD antibodies may not become commercial, and;

- The AD antibodies being sold related to brain-derived tau (see Alzheimer’s R&D: neurodegeneration and brain-derived tau).

- This FY reiterated how the approval of two AD treatments had created greater interest among IVD companies to create blood tests that identify and monitor AD:

“Recently, the approval of first generation AD therapeutics (Lecanemab jointly developed by EISAI and Biogen, and Donanemab from Eli Lilly) have changed the perception of AD therapy, and it is likely that second generation therapeutics, or combination therapies will further help to slow the disease process. Patients presenting early in the ATN [Amyloid plaques/Tau tangles/Neurodegeneration] pathway appear to benefit most from therapy. Therefore, ATN assessments can be used not only to screen for patients suitable for therapy but also for monitoring patients whilst on therapy.”

- Board remarks at the 2024 AGM provided further insight into the IVD industry’s reaction to the new AD treatments. Attendees were told:

- The emergence of AD treatments could be the “dawn of a new blockbuster era” for neurology diagnostics during the 2030s;

- “Customers see a future where there will be a whole new menu on their blood-test machines…there could be a number of different tests that tell different things about what’s happening in the brain“, and;

- The subsequent change of “customer psychology” has been “one of the most remarkable” witnessed during the last 20 years.

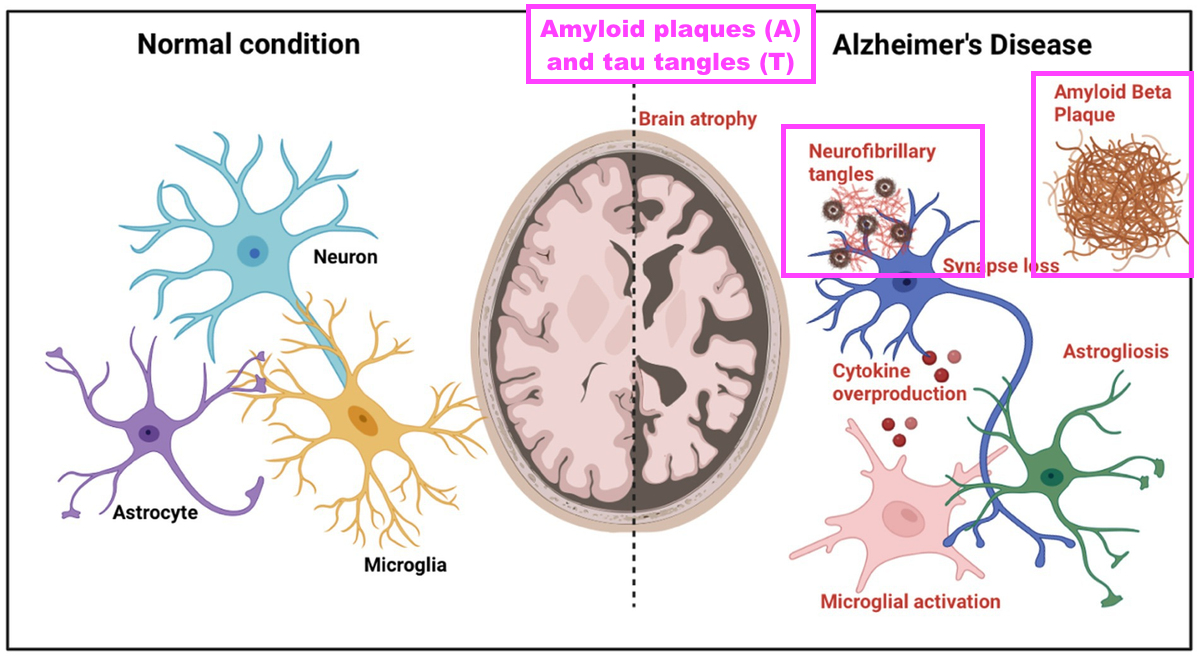

- AD is currently identified and monitored through brain scans and/or lumbar punctures, both of which — unlike simple/fast/cheap blood tests — are impractical for screening and monitoring the wider population for potential AD and any subsequent treatment.

Alzheimer’s R&D: neurodegeneration and brain-derived tau

- This FY reiterated how the onset of AD is defined through three phases of an “ATN framework“:

“Over the last few years, a considerable amount of our laboratory resource has been allocated to the Tau project and Alzheimer’s disease (AD) diagnostics. AD is a complex disease that manifests itself differently across the patient population.

At a cellular level, nerve cells (neurons) become associated with amyloid (A) plaques that build up outside the neurons. This is followed by the build-up of Tau (T) tangles inside the neurons. These pathological processes then result in neuronal cell death and the symptoms of neurodegeneration (N) that accompany this.

This “ATN” framework is used by neurologists to define the AD pathway that progresses for many years before patient symptoms become more obvious.”

- BVXP appears to enjoy a favourable R&D position within the neurodegeneration (N) part of the ATN framework:

- Neurodegeneration is the process of the brain shrinking as neurons are lost through the long-term build-up of amyloid plaques (A) and tau tangles (T):

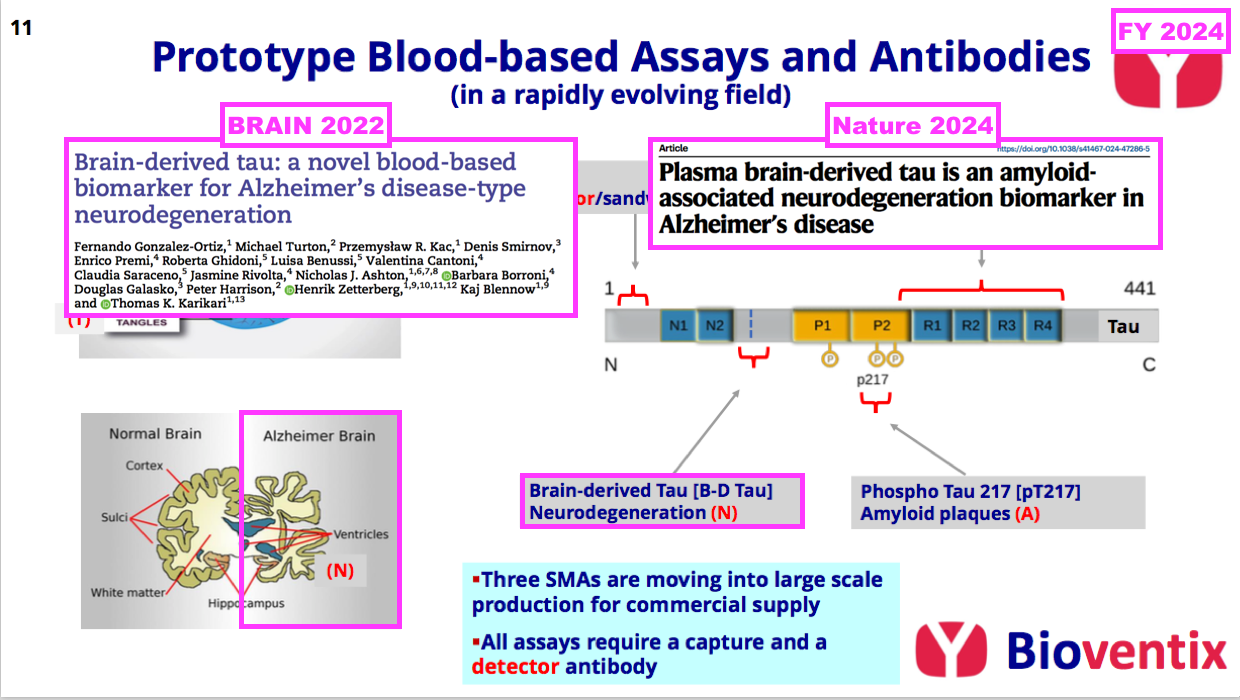

- BVXP started collaborating with the University of Gothenburg (UGOT) during early 2020 to create new antibodies for identifying and monitoring AD…

- ..and H1 2023 then announced UGOT’s first published results of BVXP’s brain-derived tau antibody:

[H1 2023] “We continue to create new antibodies which will be subjected to assay development and validation using clinical samples at the world-renowned laboratory of Kaj Blennow and Henrik Zetterberg at the University of Gothenburg. Using a novel Bioventix antibody, our academic collaborators in Gothenburg have recently published data on a novel assay that detects “brain-derived” Tau in blood (Brain 2022: 00; 1-14).”

- H1 2023 also noted brain-derived tau could be a “useful” indicator of neurodegeneration (N):

[H1 2023] “Brain-derived Tau levels in blood appear to mimic Tau levels in cerebral spinal fluid and could be a useful blood biomarker for neurodegeneration that occurs later in the Alzheimer’s disease pathway.”

- My layman interpretation of the associated BVXP/UGOT scientific paper — “Brain-derived tau: a novel blood-based biomarker for Alzheimer’s disease-type neurodegeneration” (published December 2022) — derived the following conclusions:

- Brain-derived tau in blood seems able to replicate the established AD-identification qualities of spinal-fluid tau, and;

- Unlike alternative indicators of neurodegeneration (such as neurofilament light), brain-derived tau in blood can differentiate between AD and other neurological disorders.

- The associated scientific paper even claimed brain-derived tau in blood could “complete” the ATN framework for AD blood tests:

[BRAIN 2022] “Brain-derived tau is a new blood-based biomarker that outperforms plasma total-tau and, unlike neurofilament light, shows specificity to Alzheimer’s disease-type neurodegeneration. Thus, brain-derived tau demonstrates potential to complete the AT(N) scheme in blood, and will be useful to evaluate Alzheimer’s disease-dependent neurodegenerative processes for clinical and research purposes.”

- Two further BVXP/UGOT scientific papers on AD neurodegeneration have since been published:

- “Levels of plasma brain-derived tau and p-tau181 in Alzheimer’s disease and rapidly progressive dementias” (published September 2023), and;

- “Plasma brain-derived tau is an amyloid-associated neurodegeneration biomarker in Alzheimer’s disease” (published April 2024).

- My layman interpretation of both papers concluded brain-derived tau in blood can successfully identify patients with greater immediate risk of neurodegeneration through AD beyond a pure pTau181/pTau217 test (see Alzheimer’s R&D: amyloid plaques and pTau)

- My online searching for ‘brain-derived tau‘ has found only one source of non-BVXP/UGOT scientific papers — an investigation of how brain-derived tau extracted from brain tissue contributes to different neurodegenerative disorders, including AD.

- All my other searching for ‘brain derived tau‘ refers only to BVXP and BVXP/UGOT-related scientific papers, which suggests BVXP still retains some sort of R&D edge with this particular AD project.

- I therefore speculate BVXP’s TauJ.5H3 brain-derived tau antibody is more likely to become a commercial success than the company’s other AD work.

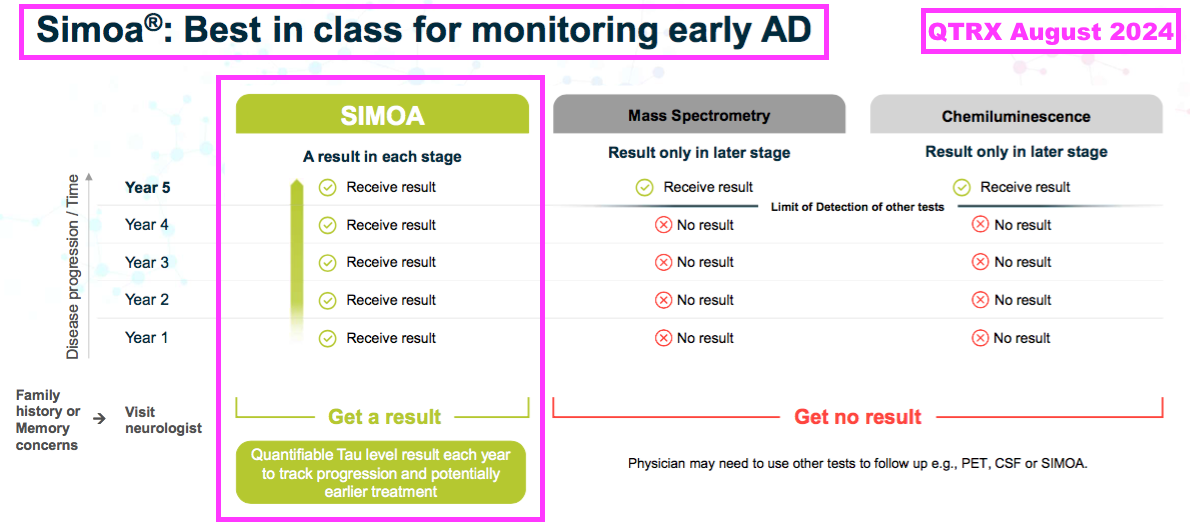

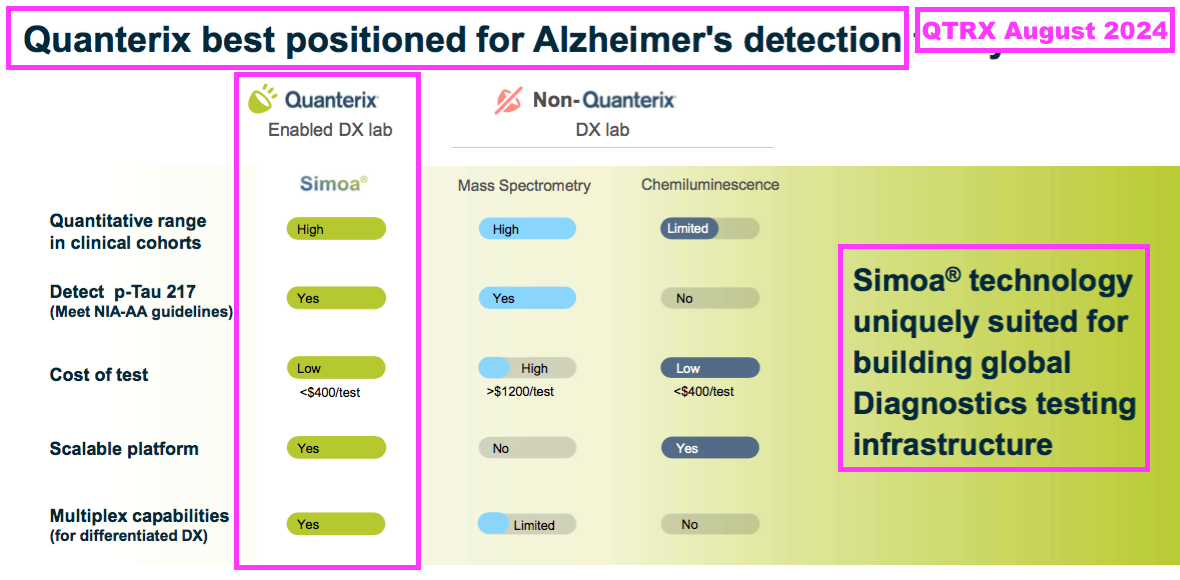

- The most visible validation of brain-derived tau is through Quanterix (QTRX):

- QTRX is a $371m Nasdaq-quoted manufacturer of “ultrasensitive” immunoassay analysers, which are apparently “up to 1000x” more powerful than conventional analysers:

- QTRX reckons its machines are the equipment of choice for AD research:

- QTRX currently promotes BVXP’s brain-derived tau at the top of its website:

- This FY confirmed the antibodies sold through QTRX contributed towards the £155k AD revenue:

“In additional to our conventional IVD customers, we have also supplied antibodies to specialist platform customers, for example Quanterix Corporation who specialise in assays for the research market. The research market is established earlier than more regulated tests for routine clinical use and it is pleasing that royalty revenues from such activities have already been established.

…

“Whilst our major IVD customers’ primary interest is in developing regulated tests for routine clinical use, expert neurology centres are already adopting “research use only” tests in advance of the availability of other tests through hospital-orientated IVD companies. Some of these R&D tests are run on Quanterix Corporation (Billerica, MA) machines and our partnership with Quanterix has resulted in one commercial R&D test for neurodegeneration (N) that uses an SMA and which has generated on-going royalty revenues.“

- Board remarks at the 2024 AGM provided further insight into brain-derived tau. Attendees were told:

- The associated antibodies are “well placed” because “they are good” and “we kind of got there first“;

- Other antibody developers have had two years to “make antibodies that look like ours“;

- A patent was considered, but the idea of brain-derived tau already featured in a Japanese patent, and;

- The vast majority of the £155k AD revenue is through physical sales to IVD companies, with only “modest” income from QTRX royalties.

- Brain-derived tau was discussed briefly during this 2024 QTRX interview with UGOT-professor Henrik Zetterberg: (from 14:00):

Alzheimer’s R&D: amyloid plaques and pTau

- I am not convinced BVXP enjoys a favourable R&D position within the amyloid plaques (A) part of the ATN framework.

- The comparable FY stated:

[FY 2023] “A leading blood biomarker for “A” is a phosphorylated form of tau called pTau217. A prototype assay from Gothenburg using an SMA has now been established which has performed well with frozen patient samples from a number of different cohorts. The “effect size” (AD patients relative to controls) has been x2-4 which is similar to other leading groups and likely to be clinically useful. The percentage of false positives and false negatives is also relatively modest confirming potential clinical utility.”

- The comparable FY had directed shareholders to this UGOT/BVXP scientific paper about pTau217: “A novel ultrasensitive assay for plasma p-tau217: performance in individuals with subjective cognitive decline and early Alzheimer’s disease“ (published October 2023).

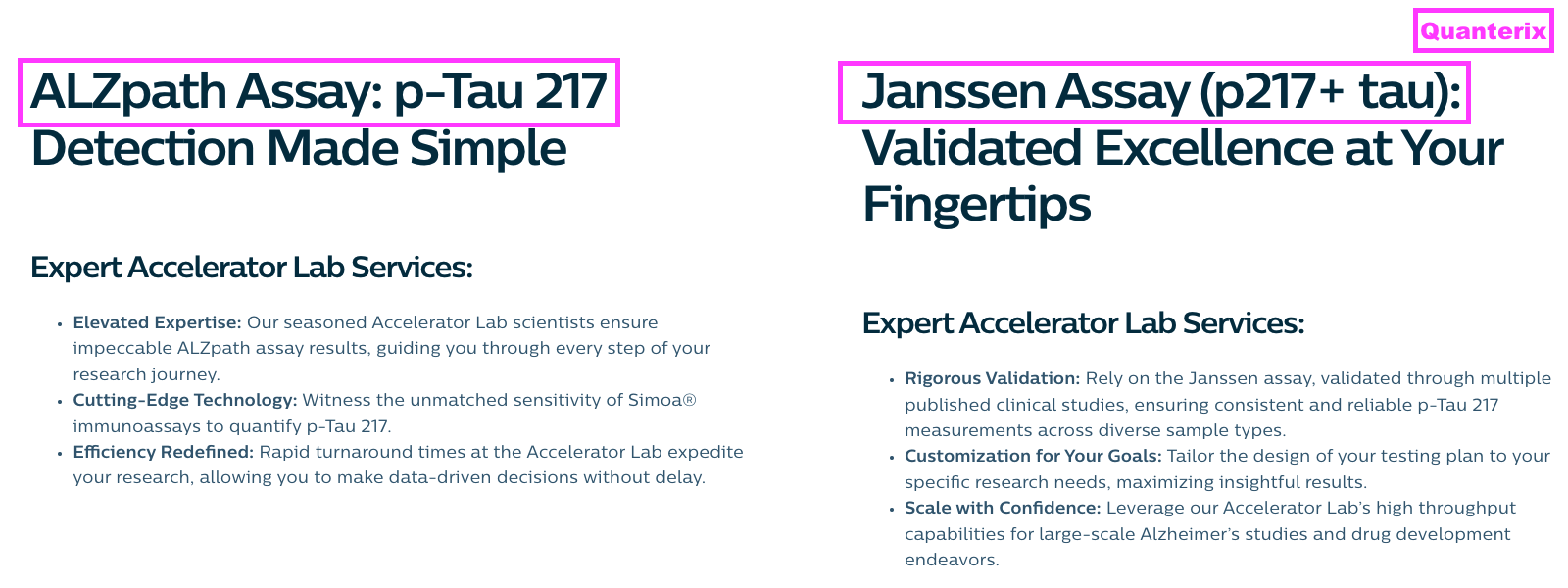

- However, BVXP is one of many antibody developers that has worked on a pTau217 test for detecting the early onset of AD through the build-up of amyloid plaques. The preceding H1 name-checked a few competitors:

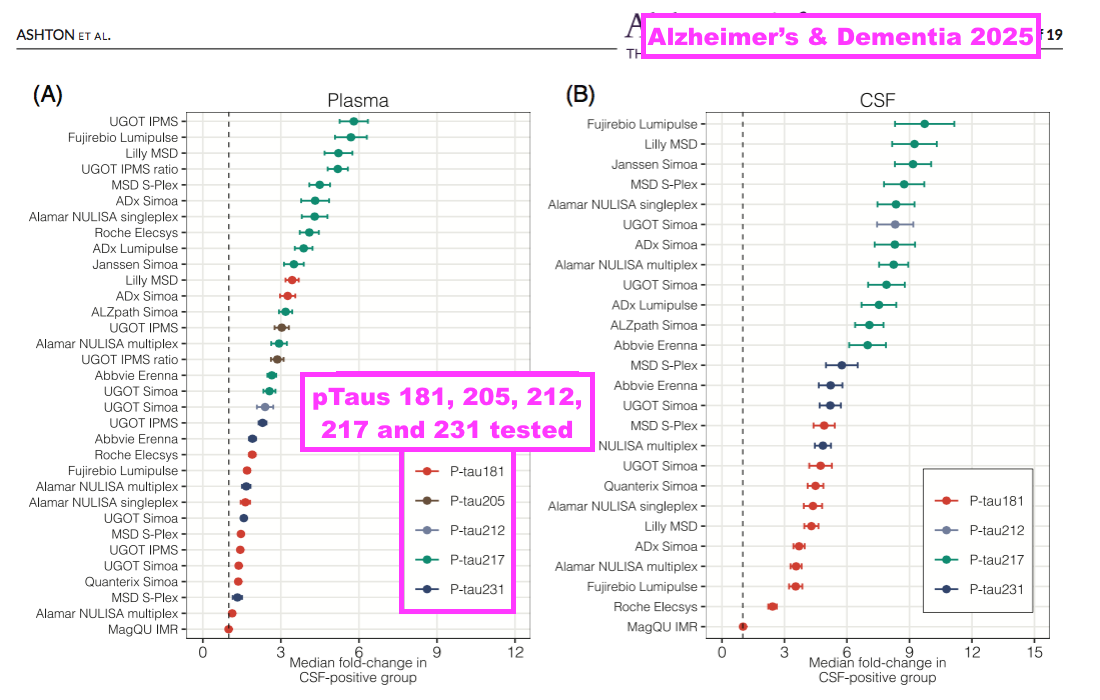

- The scale of the pTau217 competition is reflected by the scientific paper “Alzheimer’s Association Global Biomarker Standardization Consortium (GBSC) plasma phospho-tau Round Robin study” (published February 2025), which was prepared in part by UGOT and reported the outcome of 31 different pTau antibody tests.

- Of the 31 different tests, 13 involved pTau217 and suppliers included Abbvie, ADx, Alamar, ALZpath, Eli Lilly, Fujirebio, Janssen, Meso Scale, Roche and UGOT (using BVXP’s pTau217 antibody!):

- The study concluded pTau217 remains the pre-eminent epitope for indicating the early onset of AD versus alternatives such as pTau181 and pTau213:

[Alzheimer’s & Dementia 2025] “This study, of the largest number of p-tau assays to date, provides more evidence that assays targeting p-tau217 using several different methodologies show good agreement with one another, and consistently demonstrate greater fold-change in AD versus non-AD groups than those targeting other p-tau forms. These results show that this is not fundamentally predicated on a single analytical platform, or assay design.

These findings confirm that plasma p-tau217 may have clinical utility in determining the presence or absence of AD pathology in symptomatic individuals, which is relevant in the era of disease-modifying therapies.”

- BVXP’s pTau217 test — now named UGOT pTau217 — was the first pTau217 test to be developed for “pure academic interests” and wider research purposes:

[Alzheimer’s & Dementia 2023] “Even though plasma p-tau217 assays on different platforms from some biotechnology/pharmaceutical companies are expected to become commercially available in the next few months, having an assay developed completely from an academic source removes restrictions such as the need to have the results cleared by the company in question before data can be published. Moreover, the companies tend to select cohorts with clinical and biomarker characterisation that align with their commercial interests, thereby limiting access to these assays. Getting rid of these limitations by providing access to a plasma p-tau217 assay with pure academic interests opens the possibility for assay testing and optimisation in real-life scenarios.”

- “Pure academic interests” implies revenue from UGOT pTau217 will not be significant for BVXP.

- Board remarks at the 2024 AGM provided additional pTau217 insight. Attendees were told:

- “We are well behind a company called ALZpath“;

- Any pTau217 revenue is likely to be “modest“, and;

- “One or two” customers have concluded pTau217 testing, and BVXP has not been included in their final selection (“Some ships have already sailed… We were too late to get in“).

- Management comments during November’s ShareSoc seminar confirmed ALZpath leads the pTau217 field:

[BVXP seminar 2024] “There’s competition from people that have been in the field longer than we have. There’s a company called ALZpath, who have got a really good pTau217 antibody that’s really difficult to compete with.”

- The aforementioned study of 31 pTau tests provided some encouragement about BVXP’s brain-derived tau antibody:

[Alzheimer’s & Dementia 2025] “Caution must be taken not to over interpret the meaning of absolute values of plasma p-tau. Peripheral factors may also come into play in increased plasma p-tau levels, and unexpectedly high plasma p-tau values can also be observed in a single timepoint in healthy individuals followed over several weeks and in N-terminal assay designs. Other more brain-specific tau biomarkers such as brain-derived tau (BD-tau) or assays that are more reflective of tau pathology may provide further information in this context.”

- The text suggested combining tests for pTau217 and brain-derived tau could provide a more accurate assessment of the patient’s AD status.

- I note the study of 31 pTau tests provided a single footnote to brain-derived tau, which referred to the aforementioned BVXP/UGOT scientific paper “Brain-derived tau: a novel blood-based biomarker for Alzheimer’s disease-type neurodegeneration” and implied BVXP’s brain-derived tau may not yet face any blood-test alternatives.

- The study of 31 pTau tests included one test for pTau212:

[Alzheimer’s & Dementia 2025] “In total, 31 single p-tau measurements (11 p-tau181, 1 p-tau205, 1 p-tau212, 13 p-tau217, and 5 p-tau231) across eight immunological platforms were compared.“

- The pTau212 footnote referred to the BVXP/UGOT scientific paper “Plasma p-tau212 antemortem diagnostic performance and prediction of autopsy verification of Alzheimer’s disease neuropathology” (published March 2024), for which BVXP supplied the pTau212 antibody.

- BVXP has participated within one further pTau212 UGOT scientific paper — “Plasma p-tau212 as a biomarker of sporadic and Down Syndrome Alzheimer’s disease” (pre-printed November 2024) — which indicates BVXP’s antibody successfully detects the onset of AD within patients with Down Syndrome.

- BVXP has participated within one pTau217 scientific paper and one pTau181 scientific paper, but has now has been involved with two pTau-212 scientific papers.

- The implication perhaps is BVXP has found an R&D niche with pTau212 and Down Syndrome, a condition that eventually develops AD.

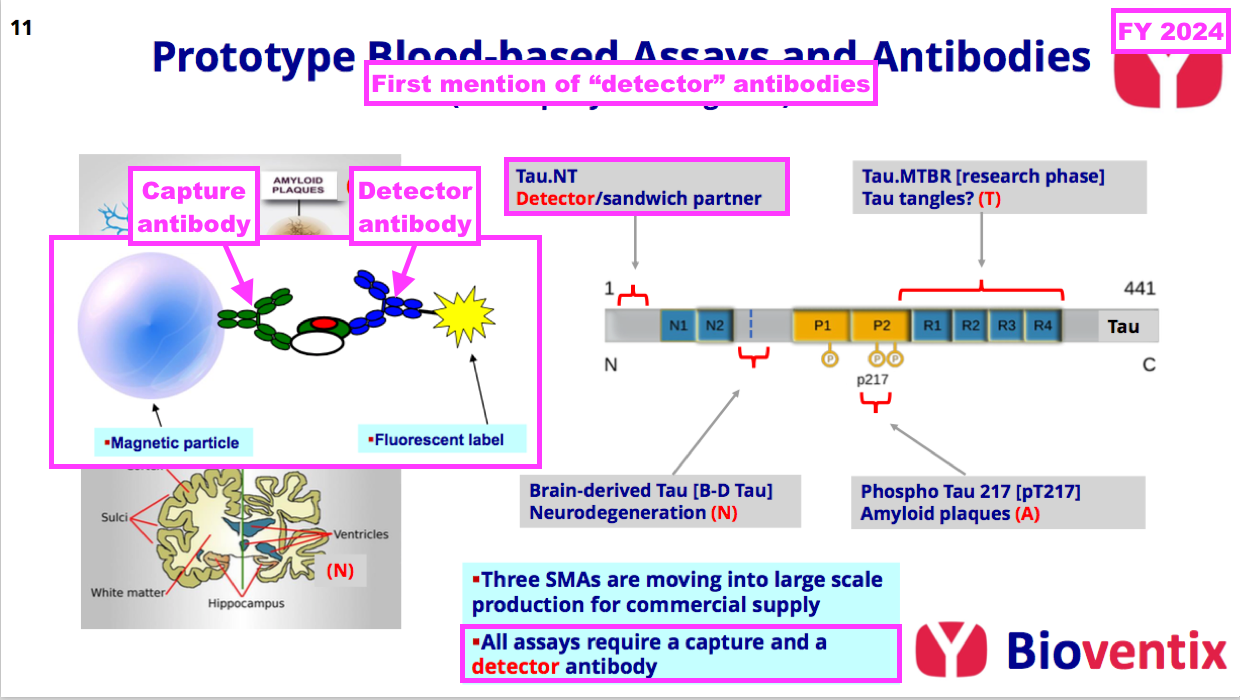

Alzheimer’s R&D: tau tangles and detector antibodies

- BVXP’s present R&D position within the tau-tangle (T) part of the ATN framework is hard to determine.

- This FY just referred to a “research phase” for developing antibodies to detect the build-up of tau tangles:

- Management comments during November’s ShareSoc seminar were quite vague on the company’s tau-tangle R&D:

[BVXP seminar 2024] “We haven’t quite worked out with our esteemed friends in Gothenburg exactly if any of the targets that we’re going for in this MTBR [microtubule-binding region] are of use. And that’s going to be ongoing. I can see us working on Tau well into next year, probably towards the end of next year.”

- Board remarks at the 2024 AGM were similarly vague. Attendees were told:

- BVXP is “creating new antibodies every day, every week” for tau-tangle R&D;

- The first news will come from UGOT, maybe during 2025, and;

- “No one’s quite sure what will work out.“

- Online searching reveals epitopes MTBR-205 and MTBR-243 within spinal fluid are possible indicators of tau tangles.

[AlzForum 2024] “Clinicians may soon have a blood test for neurofibrillary tangles. At AAIC 2024, held July 27-31 in Philadelphia, Randall Bateman, Washington University, St. Louis, reported that a fragment of tau containing the microtubule-binding region, called eMTBR-243, can be detected in plasma and that it identifies people who have neurofibrillary tangles in their brains. When combined with a plasma marker of amyloid, such as p-tau217, it could help confirm when a person has AD.”

- From what I can tell, no scientific papers confirming an accurate tau-tangle blood test have so far emerged.

- This FY announced BVXP’s work on a detector antibody for AD:

- Detector antibodies combine with capture antibodies to improve the sensitivity and accuracy of a blood test:

- BVXP has thus far been developing capture antibodies for its AD research.

- For example, the aforementioned BVXP/UGOT scientific paper “Plasma brain-derived tau is an amyloid-associated neurodegeneration biomarker in Alzheimer’s disease“ (published April 2024) reveals BVXP’s capture antibody was partnered with a BioLegend antibody:

[Nature 2024] “All biomarkers were measured on the Simoa HD-X platform. CSF and BD-tau was measured according to Gonzalez-Ortiz et al., using TauJ5.H3(Bioventix) as capture antibody and Tau12 (BioLegend, #SIG- 39416) as partner antibody.”

- Board remarks at the 2024 AGM did not shed huge light on detector antibodies for AD. Attendees were told:

- The AD tests all need a capture antibody and a detector antibody;

- Companies can mix and match different suppliers of capture antibodies and detector antibodies, and;

- A royalty will be paid on both types.

- Whether BVXP succeeds with its AD research through a tau-tangle antibody or a detector antibody — or through brain-derived tau, pTau217, pTau212 or something else — remains to be seen.

- Board remarks at the 2024 AGM summarised the general AD prospects as follows:

- “We have quite a few shots on goal“;

- “We are 99% certain that we will be selling some Tau antibodies to at least one customer.“, and;

- The scale of AD revenue — whether £thousands or £millions — will be determined by “what happens in the coming months and year“.

Other R&D

- BVXP’s other R&D efforts are becoming increasingly immaterial versus the AD work.

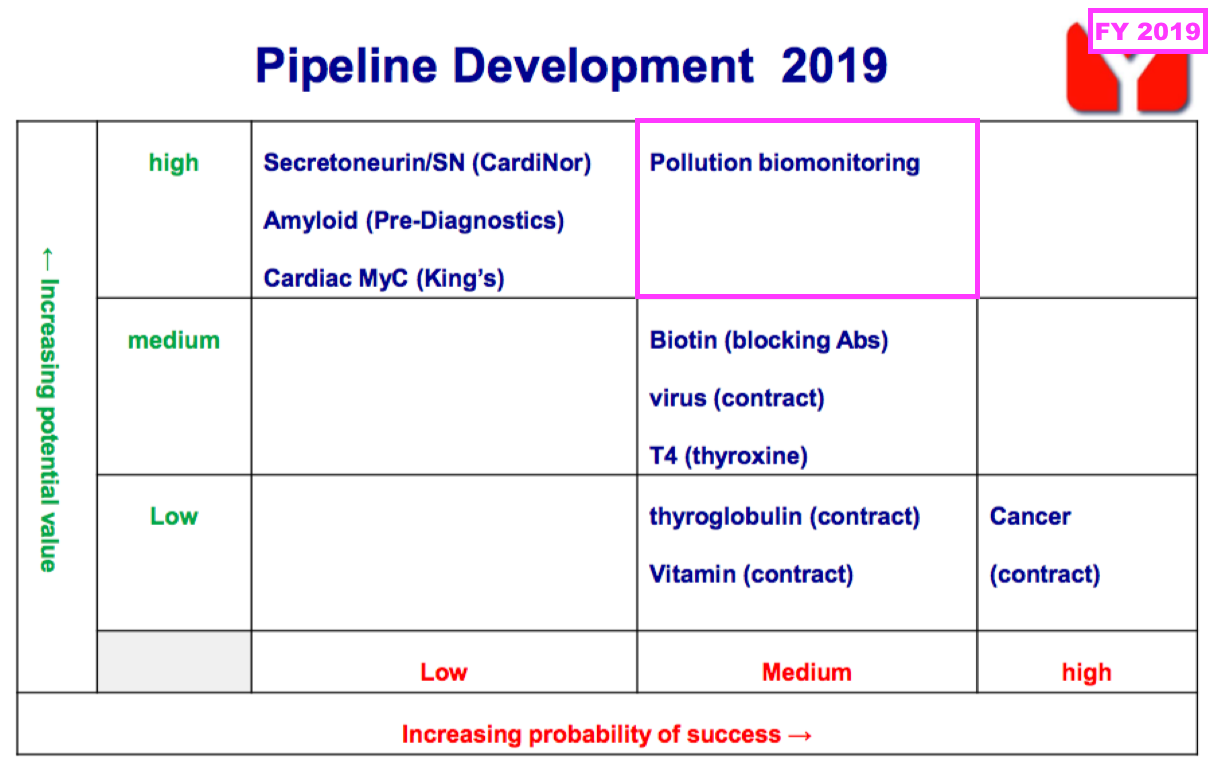

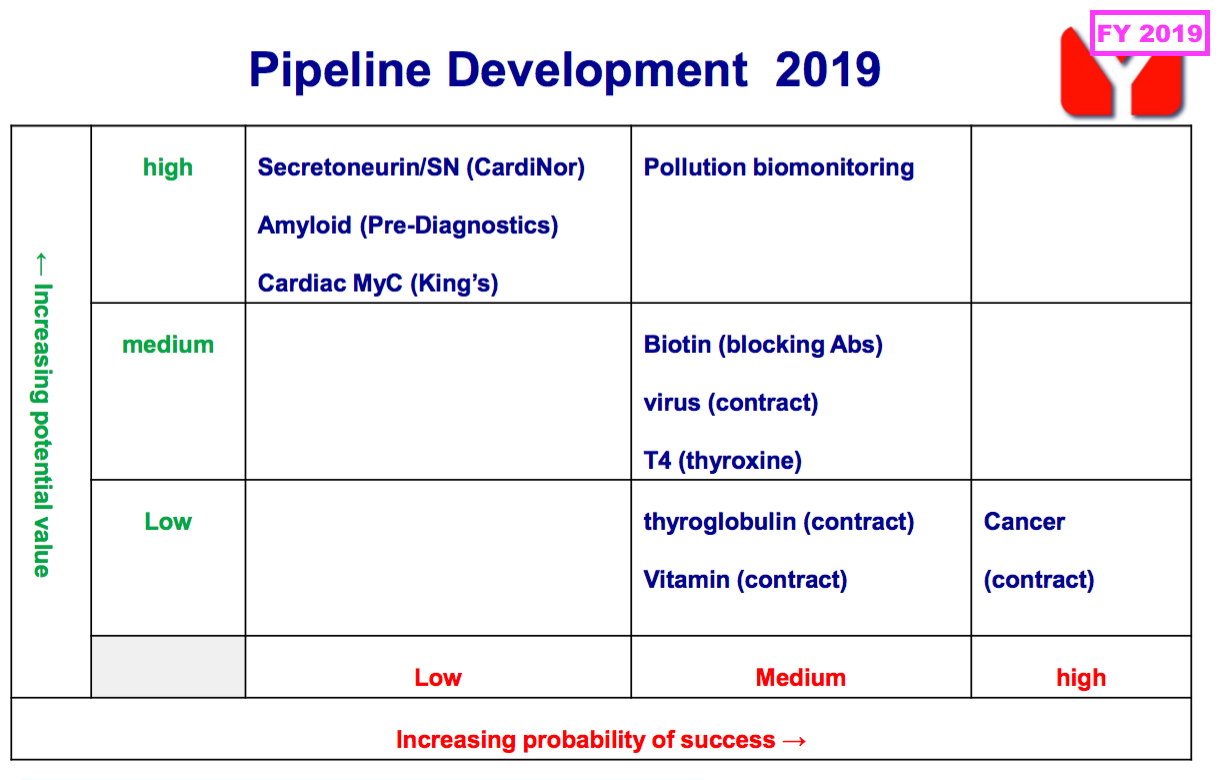

- BVXP hinted as such, as the pipeline grid that previously outlined the company’s research projects and their chances of success…

- …was absent for this FY.

- Board remarks at the 2024 AGM explained the grid was removed because it had “gone beyond its shelf life” and did not reflect how AD could be the “big value driver“.

- BVXP’s other R&D efforts fall into three groups:

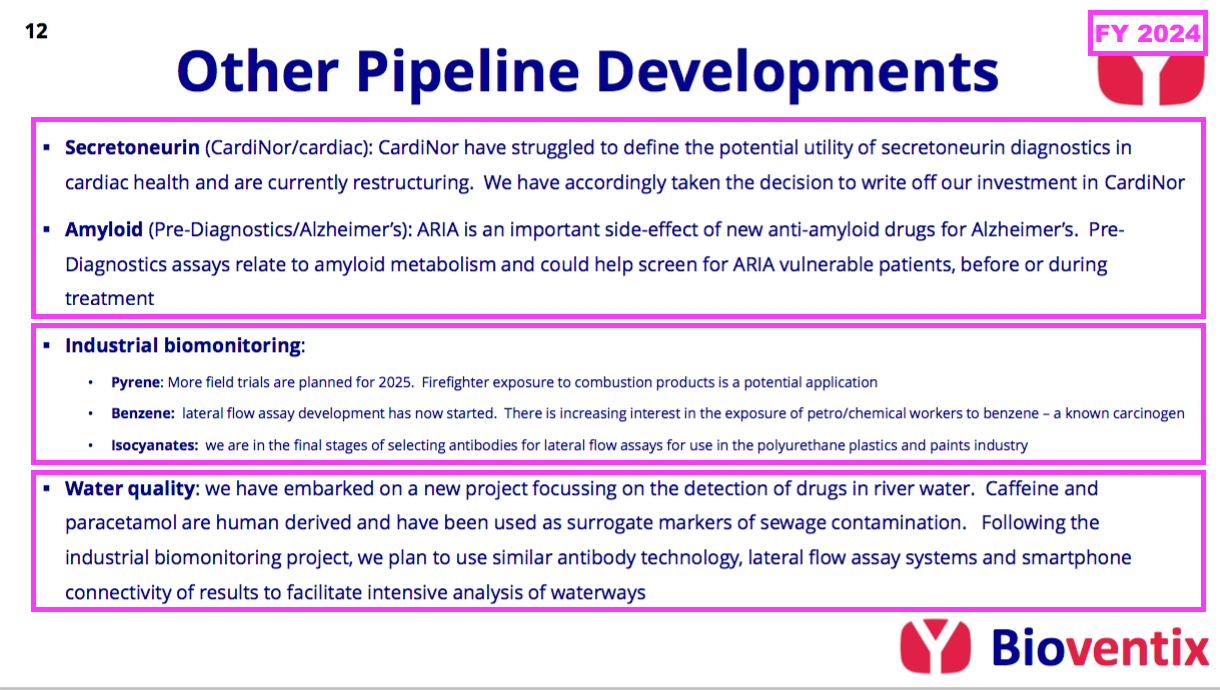

- Investments in two Norwegian blood-test research houses (CardiNor and Pre-Diagnostics);

- Three industrial-biomonitoring projects, and;

- A new water-quality project.

- The aforementioned £183k CardiNor write-off was not surprising, given another shareholder had already impaired its investment.

- Management comments during a 2016 ShareSoc seminar did warn CardiNor had “modest at best” prospects:

[BVXP seminar 2016] “I would emphasise the risk for anything that is new and unproven and not recognised by the global medical community. That is by definition high risk.

And so you can have a spreadsheet which will tell you that global heart disease and diagnostics are enormous, but the probability of this [CardiNor research] actually being on the market in 10 years’ time, I would have to admit that that’s modest at best… I do not add this to my spreadsheet and I would recommend that other people don’t.”

- The CardiNor write-off reduces BVXP’s investments to just Pre-Diagnostics, which is studying the side effects of AD treatments and has ominously not updated investors publicly since 2023. BVXP’s Pre-Diagnostics investment is valued at its £427k cost.

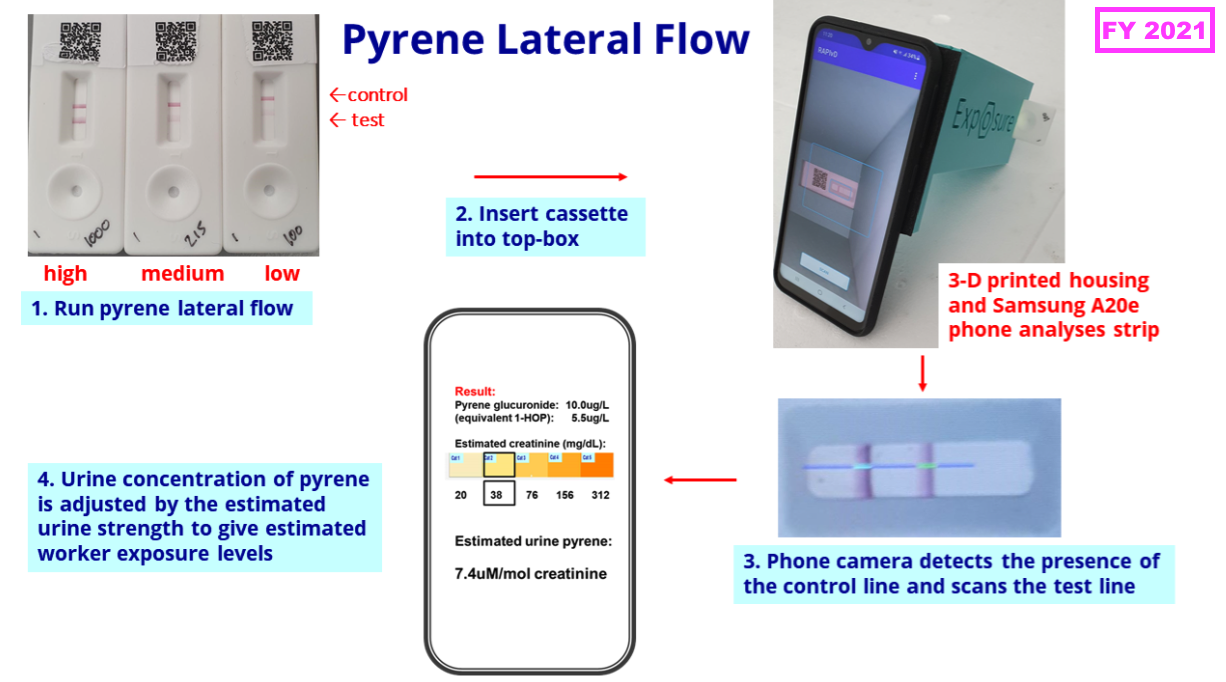

- FY 2019 first disclosed the company’s industrial-biomonitoring R&D:

- FY 2021 then outlined the kit required for an industrial-biomonitoring test:

- This FY confirmed the first biomonitoring project was still conducting trials:

“Our pyrene lateral flow system for industrial pollution biomonitoring is proceeding steadily as planned. We have now completed a second manufacturing batch of lateral flow cassettes and intend to conduct a field trial with firefighters during 2025. The follow-on project for benzene exposure has also progressed and lateral flow assay development has recently commenced.”

- Whether any of the three biomonitoring tests — for pyrene, benzene and isocyanates — becomes commercial remains to be seen.

- For perspective, BVXP’s AD work commenced after the start of the biomonitoring work, yet has already earned revenue of £155k.

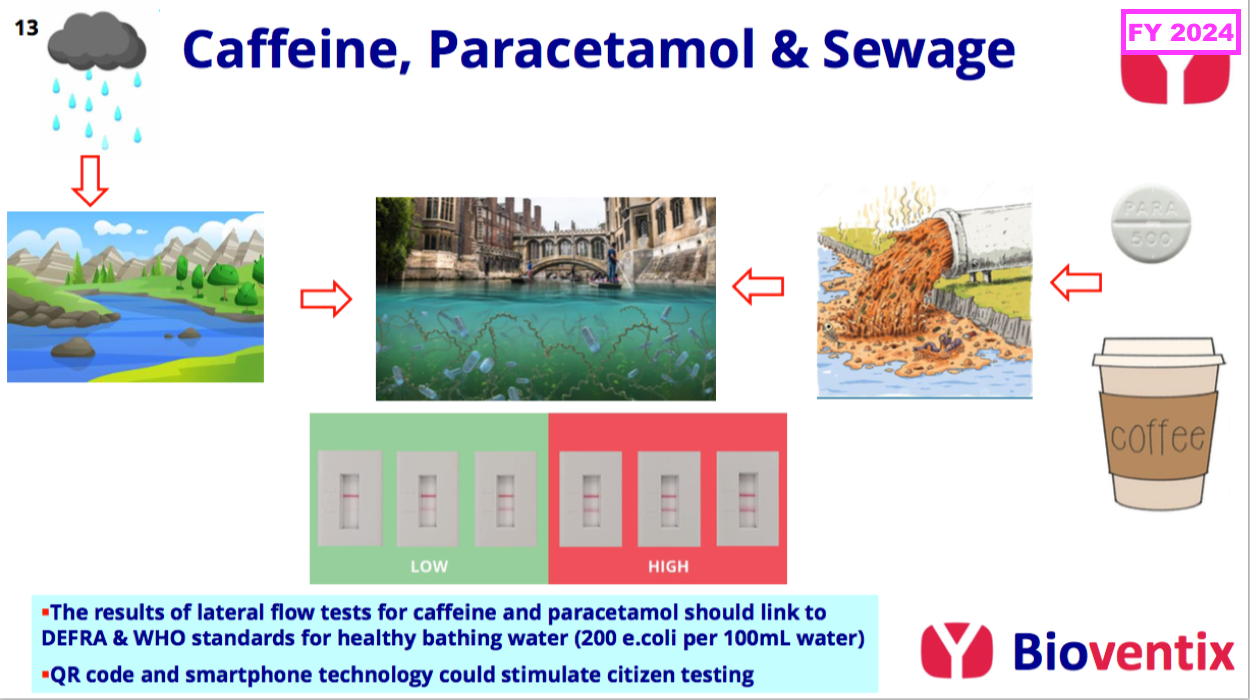

- This FY announced a new water-quality project that will “harness our experience with ‘sandwich’ antibodies, lateral-flow systems, together with phone-app technology, to facilitate rapid riverside tests”:

- An unfavourable theme of BVXP’s water-quality project and the other R&D is that no in-house blood-test work is involved.

- Such in-house blood-test R&D led to vitamin D transforming the company’s progress ten years ago…

- …and perhaps will lead to the aforementioned AD antibodies transforming the company’s progress during the next ten years.

- Management comments during a 2024 ShareSoc seminar included some slightly alarming references to the relative competitiveness of BVXP’s research technology:

[BVXP seminar 2024] “Reverse engineering is increasingly easy. But also, while we have been around for 20 years, antibody technology has raced ahead.

Twenty years ago, I think our technology was quite special, but I think that’s less so now.

There is a lot more antibody technology competition full stop. I think the ability of people not just to copy our antibodies, but to make ones better than our older antibodies, is much more the reality of being in 2024.

What protects our historic business is that it’s still a bit of an annoyance, or more than that, for someone to change an antibody, even if it’s a bit better… Because this [industry] is regulated, switching antibodies is something that people would reluctantly do.

So I think our historic business is quite well protected through this immense inertia of continual use.

For the future and new projects like Tau and Alzheimer’s, that’s a bit more of a blank sheet of paper. And we’re going into bat making antibodies for Tau against people with 2024 technology. And we’re still a little bit 1980s.

But we do things to improve and compete as best we can. Competition is an issue, particularly for new projects.”

- I speculate the absence of in-house blood-test R&D beyond AD may be due to the company utilising antiquated antibody technology.

- Certainly BVXP’s capex — just £16k during this FY — does not suggest the company is continually revamping its equipment to stay competitive (see Financials: balance sheet and cash flow).

- That earlier pipeline grid from FY 2019 now provides a sobering view on BVXP’s R&D:

- Five years on, and nothing on that grid (including the biotin ‘blockers’) has since become an obvious money-spinner.

Financials: margin and employees

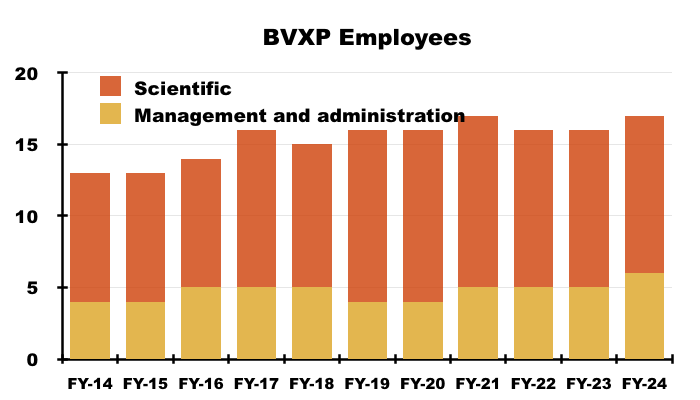

- Revenue earned from regular worldwide blood tests using antibodies developed by only 17 employees continues to translate into some wonderful accounts.

- This FY reiterated the tiny volume of physical antibodies sold:

“We currently sell a total of 15–20 grams of purified physical antibody per year, which accounts for 25–30% of our annual revenue.”

- The antibodies are sold in liquid form, and 20 grams equates to five or six litres of shipped product:

- Physical sales for this FY were as much as £4.5m, which implies antibodies may sell for an incredible £220k a gram.

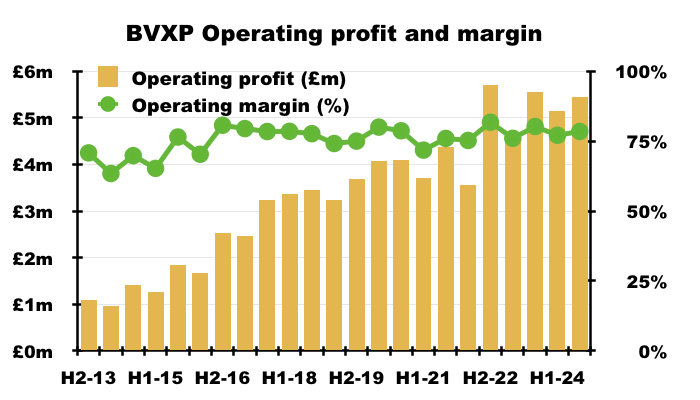

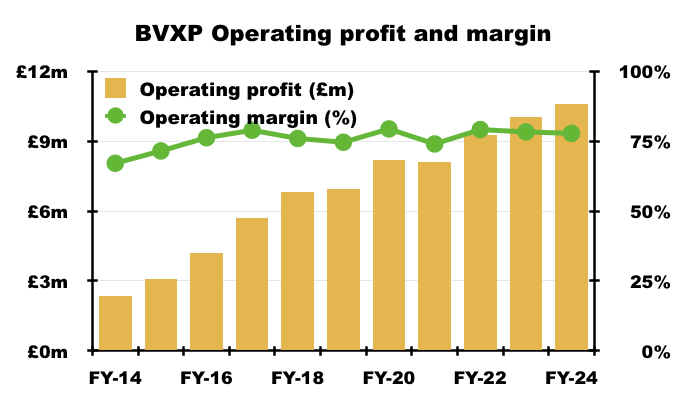

- Add in the royalty income — which attracts no direct costs — and no wonder BVXP’s operating margin has topped a remarkable 70% since H2 2015:

- Without adjustments for the troponin-revenue error and the delayed Chinese income, this FY recorded a majestic 78% margin:

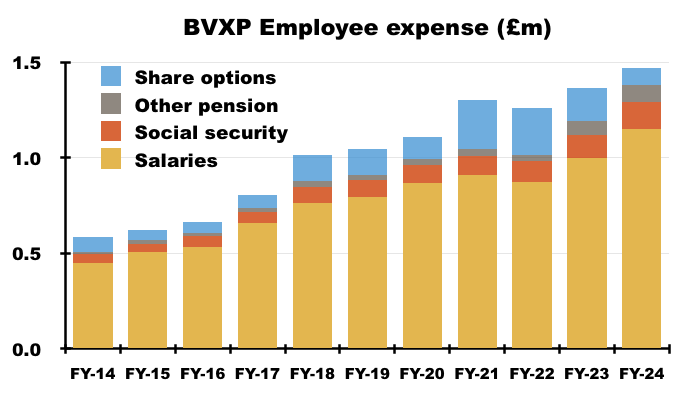

- BVXP’s largest cost continues to be its workforce, which typically represents approximately 50% of total expenses.

- Due to a lower share-option charge, total FY employee costs as a percentage of revenue remained at the sub-12% mark witnessed since FY 2017:

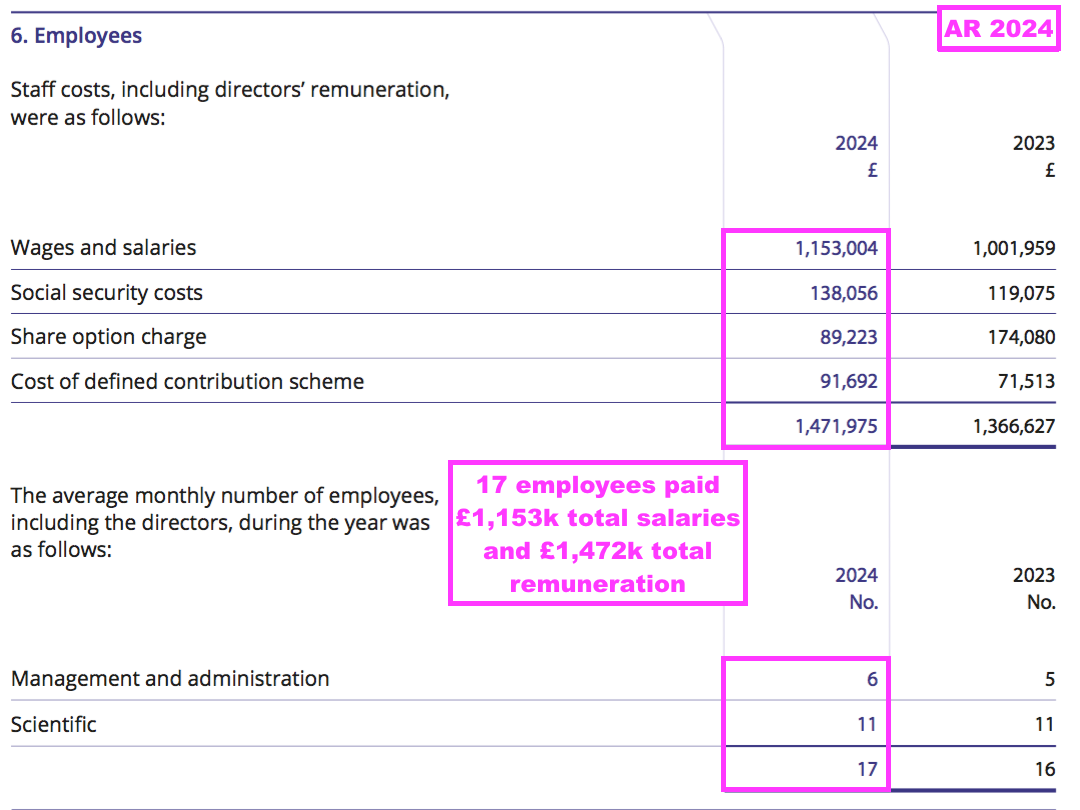

- This FY witnessed total employee salaries gain 15% to £1,153k, or £68k each:

- Note that BVXP’s per-employee ratios are not entirely accurate because not every BVXP employee works full time:

“We are very supportive of new parents and their desire to continue to work in our business and we have four employees who work on a part-time basis having returned to Bioventix after parental leave. In addition, for those long-serving employees who wish to address their work–life balance and seek to reduce their time commitment to work, we have made adjustments to help them transition to a less than full-time role whilst still retaining valuable experience, knowledge and skill in the business.“

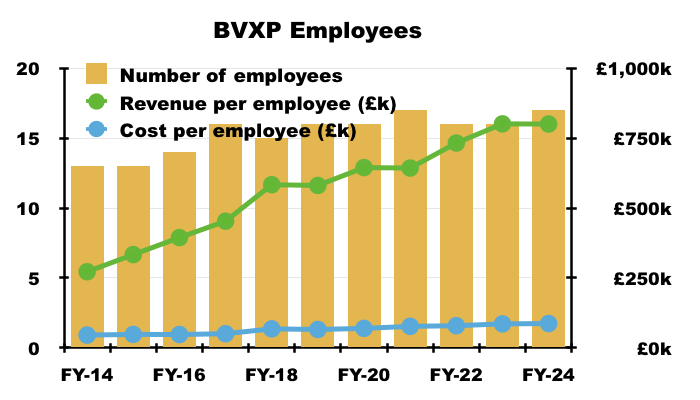

- Rising revenue per employee has in the past underlined the ‘scalable’ qualities of BVXP’s antibodies, and for this FY remained a super £800k:

- The sizeable £700k-plus gap between revenue per employee and cost per employee underpins BVXP’s majestic margin.

- This FY included new text about “competitive remuneration packages and incentive rewards”:

“We provide employees with competitive remuneration packages and incentive rewards as well as inviting them to share in the growing value of the Company through approved share options schemes. In addition, we have prioritised the wellbeing of our team and have introduced measures to support employee health and wellbeing.”

- Despite employing only one extra person, BVXP’s wage bill has advanced 45% since FY 2019, with salary per employee therefore up 37%:

- I continue to expect the workforce will receive greater salaries to reflect the significant value they have created — and may still create! — for shareholders.

- BVXP’s “incentive rewards” include share options, which are held by 16 of the 17 employees, are granted at market value, are dependent only on continued employment and represent a minor 1.5% of the share count.

- Employees for now seem very happy. This FY disclosed extended average tenures:

“Bioventix plc was established in 2003 and several of our team have been with the business for all 21 years of our existence. Across the Company the average length of service at 30 September 2024 was 11 years 11 months, an increase of 12 months since 30 September 2023. Our scientists have all been with the business for more than 5 years and our overall retention rate has been unchanged at 100% in each of the last 3 years. “

- A significant proportion of employee costs are classified as R&D, which is (commendably) all expensed as incurred and (presumably) generates only AD-related revenue at present.

- Despite this FY highlighting £200k spent on external R&D for the biomonitoring and water-quality projects, total R&D for this FY declined 17% to £1.0m:

- R&D spend of £1.0m was of course offset by the £155k earned from the AD work.

- BVXP’s R&D can — if successful! — earn astronomical returns.

- For example, BVXP’s R&D spend between FYs 2008 and 2012 was approximately £500k per annum — implying perhaps that total vitamin D R&D spend could have been up to £2.5m.

- In return for that R&D, aggregate vitamin D revenue of more than £40m has since been recorded.

Financials: balance sheet and cash flow

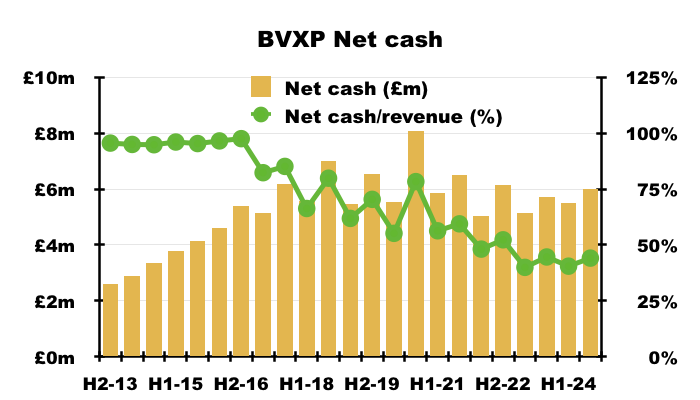

- Every year between FYs 2017 and 2023, BVXP stated a desire to maintain a £5m cash balance:

[FY 2023] “Our view continues to be that maintaining a cash balance of approximately £5 million is sufficient to facilitate operational and strategic agility both with respect to possible corporate or technological opportunities that might arise in the foreseeable future.”

- This FY did not include that text, and its deliberate removal may signal a desire to maintain much more — or much less! — than £5m.

- Cash finished this FY almost £0.2m higher at £6.0m, while the balance sheet remained devoid of bank debt, lease financing and pension complications.

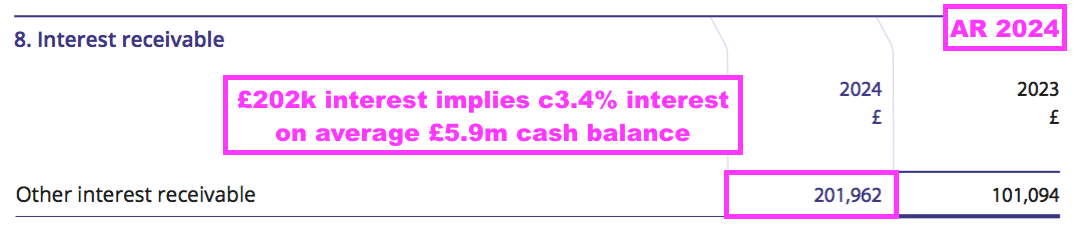

- Bank interest earned during this FY came to £202k, implying a useful c3.4% interest rate on the average £5.9m balance:

- Cash of £6m is equivalent to 44% of this FY’s revenue, which is reassuringly high compared to most quoted companies but relatively low for BVXP:

- I suppose the cash of £6m could have funded an extra £157k to maintain the H2 dividend at 90p per share.

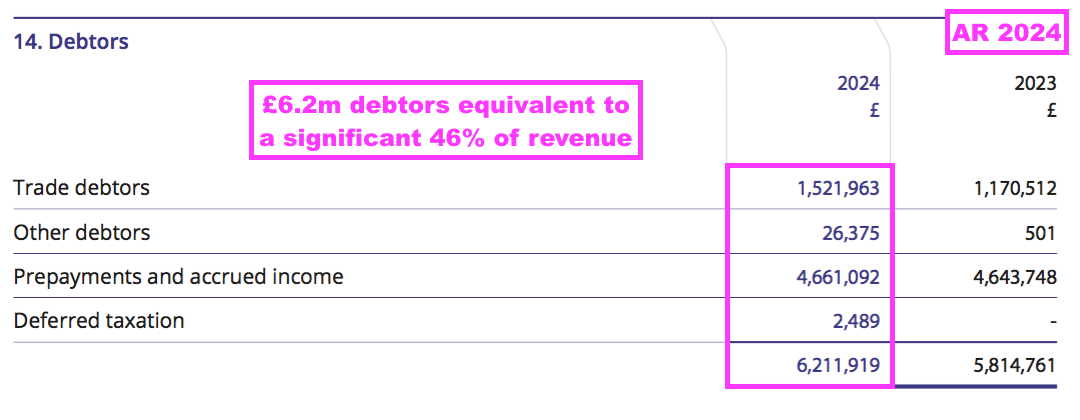

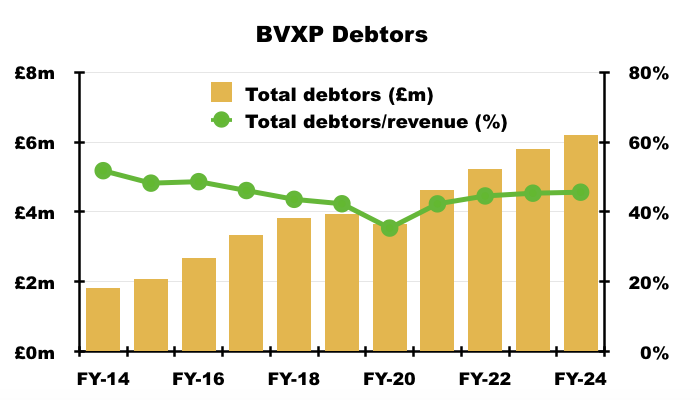

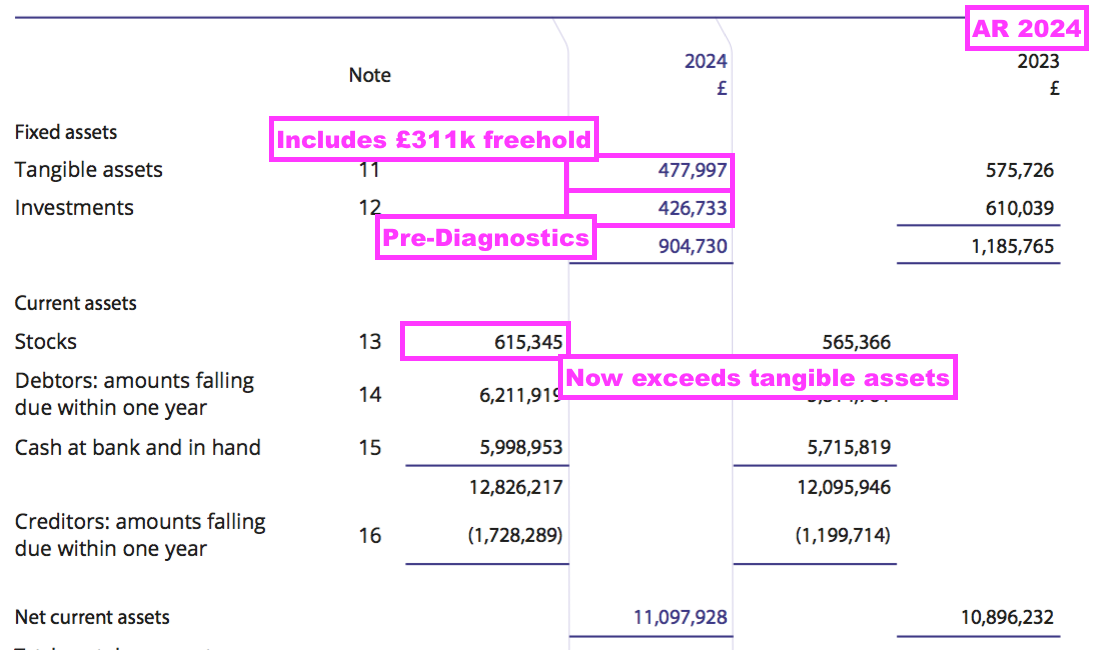

- Elsewhere on the balance sheet, total FY debtors of £6.2m do seem substantial versus revenue of £13.6m:

- Debtors mostly reflect ‘accrued income’, which in BVXP’s case are royalties recognised as revenue but have not been invoiced to the customer at the balance-sheet date. By the time BVXP publishes its accounts to shareholders, the royalties will have been paid and the accrued income already converted into cash in the bank.

- Total FY debtors were equivalent to 46% of FY revenue, which is not out of the ordinary for BVXP:

- Other balance-sheet items remain minor compared to this FY’s £10m-plus profit. In particular, tangible fixed assets — mostly the laboratory freehold — are carried at £137k less than the stock of antibodies held in the laboratory freezer:

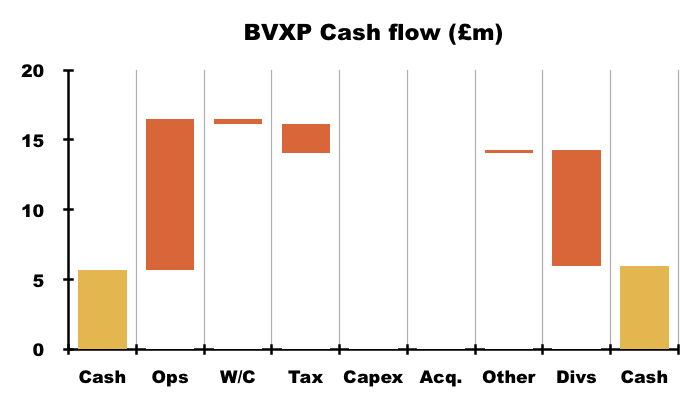

- The relatively small dependence on tangible assets was reflected by this FY’s cash flow:

- Cash from operations of £10.8m invested only £0.4m into working capital, paid tax of £2.1m and funded capex of just £16k, which allowed a hefty £8.3m to be paid as dividends.

- This FY’s cash generation extended BVXP’s superb record of converting reported profit into dividends.

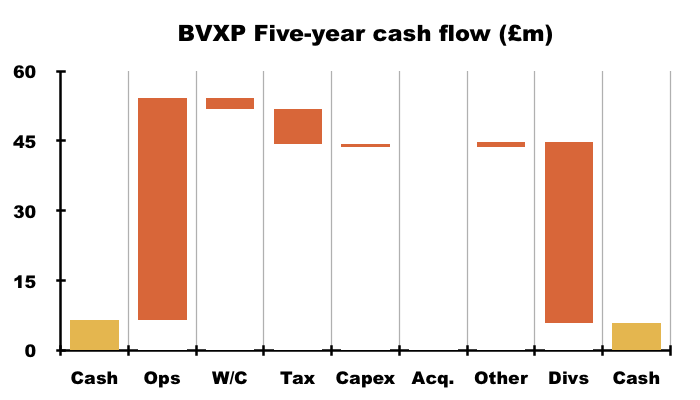

- For example, during the five years to this FY, cash declined just £0.5m after cash from operations of £47.7m invested only £2.4m into working capital, paid tax of £7.6m, funded capex of £0.6m that allowed a mighty £38.8m to be distributed as dividends:

- The aforementioned rising revenue/profit record alongside paying significant dividends emphasise how BVXP can seemingly grow with minimal reinvestment.

- Since FY 2014 for example, BVXP has declared aggregate earnings of £12.08 per share, of which £11.89 were distributed as ordinary or special dividends and the remaining 19p per share retained within the business:

- Distributing such significant dividends has made BVXP’s incremental returns on retained earnings quite special.

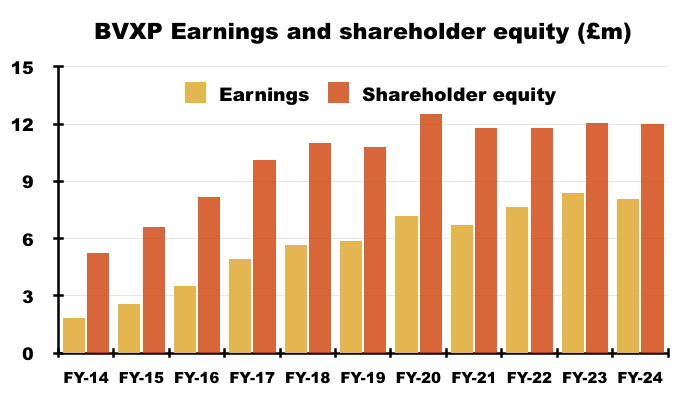

- For instance, since FY 2019 BVXP’s earnings have advanced £2.2m to £8.1m while shareholder equity (i.e. cumulative earnings less all dividends paid) has advanced £1.2m to £12.0m:

- Retaining £1.2m to enhance earnings by £2.2m over five years underlines the very attractive economics of commercial antibodies.

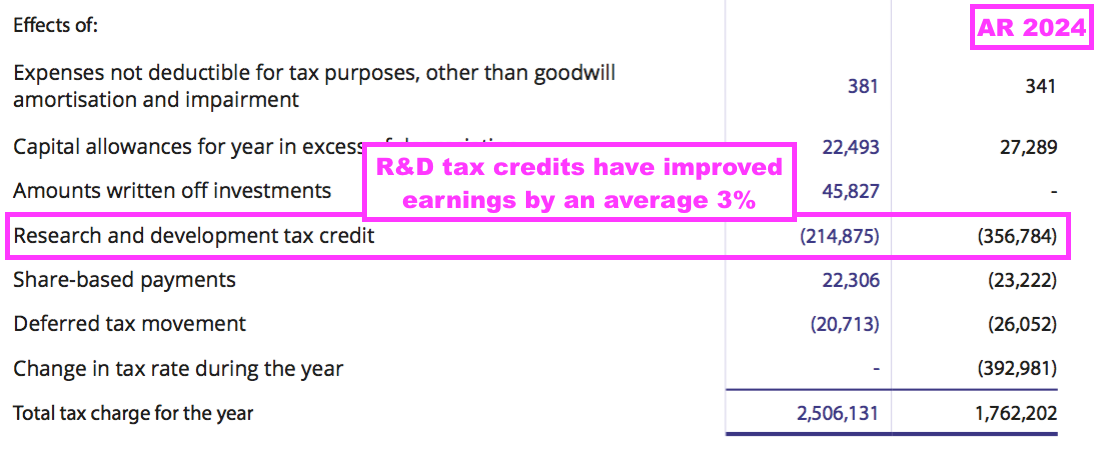

- R&D tax credits have assisted BVXP’s earnings over time, with an aggregate £1.2m awarded during the last five FYs that has boosted reported earnings by 3%:

Valuation

- This FY supplied a positive outlook for the AD research:

“We are pleased with our financial results for the year, which we believe reflect steady growth in the use of our established products in more mature diagnostic markets. We remain very encouraged by the very early signs of success for our Tau/Alzheimer’s antibodies and we look forward to more progress into the future.”

- The arrival of AD revenue during this FY led to some minor — but perhaps significant — text changes versus the comparable FY.

- In particular, the comparable FY suggested the R&D efforts could convert into revenue between 2028-2038:

[FY 2023] “Another consequence of the lengthy approval process is that the revenue for the current accounting period is derived from antibodies created many years ago. Indeed, revenue growth over the next few years from, for example the troponin antibodies, will come from research work already carried out more than ten years ago. By the same dynamics, the current research work active at our laboratories now is more likely to generate sales in the period 2028–2038.

- But the same paragraph for this FY dropped the reference to when the R&D could convert into revenue:

“Another consequence of the lengthy approval process is that the revenue for the current accounting period is derived largely from antibodies created many years ago.“

- A possible implication of this removed text is that ongoing AD revenue will now become established before 2028.

- This FY revealing vitamin D revenue growing only 1% and troponin revenue suffering customer miscalculations has left the £30 shares trading at a level first achieved during 2018:

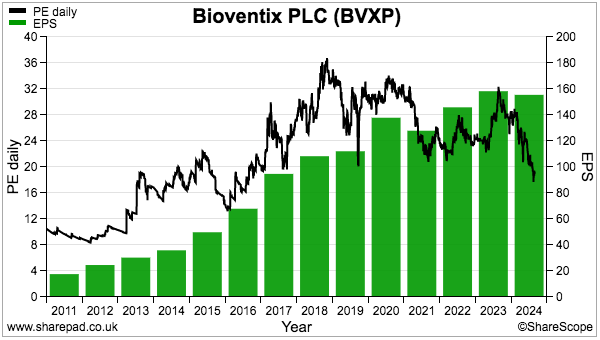

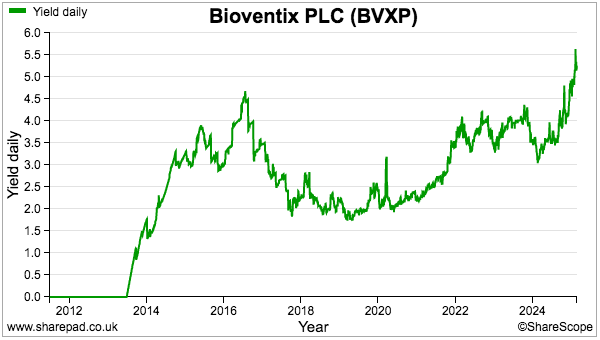

- The £30 shares trade at 19x this FY’s EPS of 155p per share:

- The 19x trailing EPS multiple is the lowest since 2016.

- Indeed, I purchased BVXP during 2016 when the £11 shares were valued at c19x trailing EPS of 57p.

- I continue to assess BVXP’s valuation through a sum-of-the-parts calculation, with the three parts being:

- Troponin:

- Vitamin D and the other core antibodies, and;

- The R&D.

- Assuming troponin revenue (from Siemens and Beckman Coulter):

- Expires entirely during 2032;

- Averages £1.5m for the next 7.5 years, and;

- Has no associated costs…

- …then aggregate earnings of troponin would be £8m after 25% standard UK tax but before any time-value discounting.

- The table below derives this FY’s possible earnings from BVXP’s vitamin D and other core antibodies by:

- Subtracting troponin revenue from this FY’s revenue;

- Then subtracting all cost of sales and administration expenses;

- Then adding back R&D costs, and;

- Then applying tax at the 25% standard UK rate:

| Estimated FY 2024 for vitamin D and other antibodies | (£k) |

| Revenue | 13,607 |

| Less troponin revenue | (1,450) |

| Less cost of sales | (926) |

| Less admin expenses | (2,097) |

| Add back R&D expense | 999 |

| Operating profit | 10,134 |

| Less tax at 25% | (2,533) |

| Earnings | 7,600 |

- Assume the R&D work has a value of zero, and my implied valuation of vitamin D and the other core antibodies is the current £157m market cap less £8m for troponin = £148m.

- £148m versus my £7.6m earnings estimate for vitamin D and the other core antibodies leads to a 19x multiple, which does not seem completely outrageous given BVXP’s antibodies enjoy:

- A competitive ‘moat’, due in part to the time/cost/upheaval of replacing established antibodies with upgraded versions;

- Recurring royalty income that can run into decades;

- Minimal overheads leading to superb margins and cash generation, and

- Collective future revenue growth perhaps in the mid-single digits.

- In contrast, assuming an R&D value of zero might be very pessimistic given:

- The AD research has led to earlier-than-expected revenue, and;

- The “large-scale production for commercial supply” of three AD antibodies…

- … all of which has very favourable implications for future AD success given the similarities with the early vitamin D sales.

- I continue to speculate a commercially popular AD antibody in a “new blockbuster era” for neurology diagnostics could become extremely valuable…

- …and I would not be surprised to see BVXP’s brain-derived tau — assuming of course it hits the big time! — one day earning revenue far exceeding the £6m currently received from vitamin D.

- This time last year, the shares traded at £50 due in part to the market’s then AD optimism…

- …and the shares revisiting £50 through renewed AD optimism — alongside collecting the annual 155p per share dividend — could combine to deliver a very useful total return during the next few years.

- While further AD progress is eagerly awaited, the shares supply a 5%-plus income for the very first time:

Maynard Paton

Thanks for a very thorough report.

https://www.youtube.com/watch?v=g0o55MIvRuY&ab_channel=Quanterix

15:55 – there are new assays coming in 1H25 for p-Tau 205 and p-Tau 212. There’s a reasonable possibility that the forthcoming Quanterix p-Tau 212 test will be powered by a Bioventix antibody given existing publications.

Hi GSBMBA99,

Many thanks for the link. I do follow QTRX on YouTube, but that video did not appear in the company’s main feed :-( Anyway, I would agree there’s (at least!) a reasonable chance the pTau212 test will have BVXP involvement. From the first BVXP/pTau212 paper https://www.nature.com/articles/s41467-024-46876-7:

“In conclusion, we have provided a pioneering demonstration that p-tau212 is a promising biomarker, tightly associated with AD pathophysiology and neuropathology. NFTs in AD brains were phosphorylated at this epitope, and a novel ultra-sensitive biomarker developed to quantify p-tau212 in blood showed similar performances to CSF p-tau212, and also plasma p-tau217.”

Indeed, would be hard to understand if BVXP were not involved with a QTRX pTau212 test given that paper refers to “pioneering” and “novel”. But I am not an expert in this field!

Maynard

Bioventix (BVXP)

Phosphorylated tau 181 and 217 are elevated in serum and muscle of patients with amyotrophic lateral sclerosis published March 2025

This is intriguing — a scientific paper that reports pTau181 and pTau217 can be detected in the blood of people with amyotrophic lateral sclerosis (ALS), which is a neurodegenerative disease that affects nerve cells in the brain and spinal cord. pTau181 and particularly pTau217 in the blood are considered signs of early-stage Alzheimer’s.

As this Alzforum article reports, confusion could now arise as to whether pTau181/217 indicates Alzheimer’s or ALS. There is also a question about whether conditions beyond ALS could also create pTau181/217 in blood.

Henrik Zetterberg of BVXP partner UGOT provides this comment on Alzforum:

“This is an amazing and very important study. There are many informative aspects to it. The p-tau increase in ALS is only seen in blood and not in CSF. This speaks strongly for phosphorylation of peripheral tau in ALS, whilst the phosphorylation in AD happens on brain-derived (short) tau, with increases in both CSF and blood.

The ALS effect is stronger for p-tau181 than p-tau217. This speaks for tau phosphorylation at amino acid 217 being a more CNS-related event; maybe this explains why p-tau217 often turns up as a slightly better biomarker for AD than p-tau181 when measured in blood.

In ALS, patients often undergo both CSF and blood biomarker analysis. The ALS pattern would be high CSF and plasma NfL concentrations, normal CSF p-tau181 concentration, and high plasma p-tau181 concentration. The study also underscores that plasma p-tau biomarkers need to be interpreted in a complete clinical context.

Phosphorylation of peripheral tau in ALS is both a problem and a possibility. Assays that combine antibodies specific against brain-derived tau with antibodies against phosphorylated tau epitopes will likely solve the problem. At the same time, blood p-tau181, especially together with NfL, may be an excellent biomarker for ALS.”

Mr Zetterberg suggests combing pTau181/217 with brain-derived tau will “likely solve the problem“. Brain-derived tau is of course BVXP’s leading AD antibody test.

Also, the Alzforum article mentions troponin:

“Strikingly, people with ALS had far more of both p-tau isoforms in muscle fibers that showed signs of atrophy than in fibers that still appeared healthy. Moreover, their serum p-tau correlated with troponin T, a marker of muscle damage. Does this mean wasting muscle fibers release p-tau181 and 217 into the blood?”

Not sure if BVXP’s troponin antibody can somehow weave itself into this ALS research!

Maynard

Hi Maynard,

Thanks for the in-depth thoughts on BVXP. It’s a stock that I have held at different times, buying back recently but unfortunately before Monday’s interim results fallout.

The financials remain supreme and I would say that the business now trades (at a market cap of around £125m) on a reasonable multiple of current, perpetual revenue streams (for the historic antibodies such as vitamin D). Albeit those historic antibodies now appear to have peaked in revenue.

The share price chart is dreadful, and I suspect it will fall further in the absence of news regarding the development of future antibodies.