26 May 2015

By Maynard Paton

Quick update on Electronic Data Processing (EDP).

Event: Interim results published 26 May.

Summary: Another rather dull update from this rather dull software microcap. These results were a little disappointing on the revenue and profit fronts, but at least there was some useful progress on the balance sheet. One day I trust EDP’s business can advance significantly and provide some long-awaited excitement. Until then I’ll just have to make do with the uncovered 7.2% dividend yield. I continue to hold.

Price: 70p

Shares in issue: 12,610,976

Market capitalisation: £8.8m

Click here for my previous EDP posts.

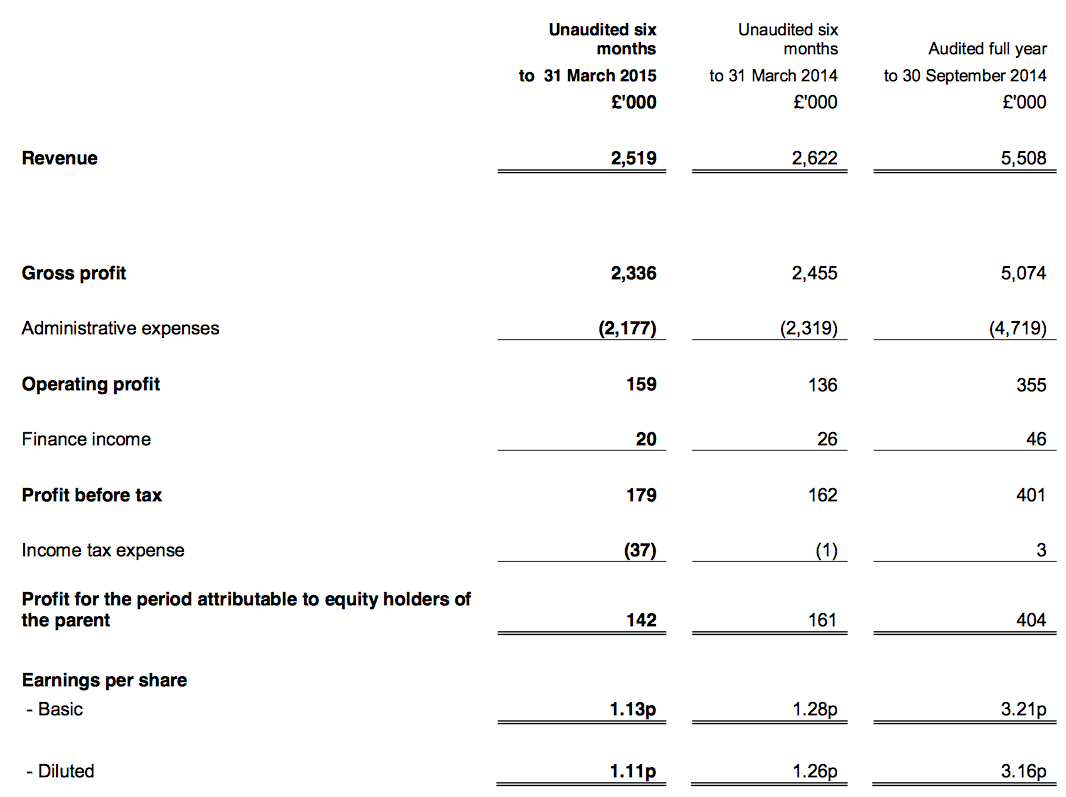

Results:

My thoughts:

* Revenue not as high as I’d hoped

I had expected EDP’s revenue to be a tad higher than the reported £2.5m.

You see, this business had for some years consistently delivered H1 and H2 revenue of around £2.8m — until the interim results of last year owned up to order delays and delivered turnover of £2.6m.

I had thought EDP’s top line had recovered following the group’s 2014 annual results, but that does not seem to be the case.

Indeed, adjusting for a recent client departure, this latest H1 revenue performance looks no better than the performance given within the disappointing comparable results of H1 2014.

At least EDP’s contracted recurring income, represented by annual software licences and hosting fees, remained high at 80% of revenue. The firm also claimed its turnover was moving towards “stronger ongoing subscription revenues”.

* Profit supported by cost savings

There was slightly better news on the profit front.

Reported operating profits gained £23k to £159k during the half, although the underlying improvement was actually £79k to £215k if you exclude redundancy costs. So, not bad.

That said… these H1 figures were in fact helped by a promised £200k of annual cost savings — so perhaps a £100k improvement ought to have been expected.

Anyway, a further £100k of savings should appear in the forthcoming H2 figures.

There was no mention this time of the possible extra £162k of annual savings that relate to EDP’s surplus properties. These costs were referred to within the last annual results and I’m hopeful EDP can soon sell the properties concerned and enjoy the additional savings quickly.

* Better progress with cash and property

I’m pleased there has been some progress with EDP’s surplus properties, with the firm recently accepting an offer for its warehouse in Sheffield. This unit is in the books at £301k.

(EDP’s other surplus property, located in Milton Keynes, is in the books at £1.4m).

Cash flow during H1 looked useful, with my calculation of surplus net cash coming in at £3.4m — about £300k ahead of the preceding year-end position. Throw in those surplus properties as well and I arrive at surplus net cash and property of almost £5.1m or 40p per share.

* New product releases underpin confident outlook

It was good to see EDP still using the word “confident” in its outlook statement — it had gone missing for a few years prior to 2014. Anyway, the chairman said:

“Whilst we expect trading conditions to remain competitive, with our continued investment in our key products and robust business model, we remain confident about the outlook for the remainder of the year.”

The “continued investment” will results in new releases of EDP’s main products in H2, which I suppose may provide a fillip to revenue. As I mentioned in my February EDP write-up, this business must improve its stagnant sales to really revive the share price.

Talking of which…

* My sums continue to point to a single-digit P/E

The obvious valuation measure remains the dividend. EDP reconfirmed its ambition of paying 5p per share for the full year, which the group kindly mentioned within its results would give a yield of 7.2%.

On a profit basis, the least I expect for the full year is a doubling of this underlying H1 performance. That would support an operating profit of £430k, which when added to the prospective property savings of £162k would give £592k.

Applying a standard 20% tax rate would in turn produce earnings of 3.8p per share — not enough to cover the promised 5p dividend.

Nevertheless, strip out the 40p per share of surplus cash and properties from the 70p share price, and EDP’s enterprise value (EV) comes to 30p per share. The P/E on my EV and earnings calculations is therefore 30p/3.8p = 8.

I must add that EDP’s H2 profits are generally stronger than its H1 profits, so in reality we could be looking at a possible underlying P/E closer to 7.

* Next update — probably annual results in December. Ex-div 2 July, 2p dividend paid 3 August.

Maynard Paton

Disclosure: Maynard owns shares in Electronic Data Processing.

EDP:

Nice to see Oleson Value lift its stake to beyond 5%:

http://www.investegate.co.uk/elec-data-process—edp-/rns/holding-s–in-company/201501090700107052B/

Oleson last confirmed its holding in January 2015 at 561,000 shares, so it has added an extra 100,000 shares since then to represent 5.25%. Alongside Boyles (18.05%) and Ewing Morris (5.15%), the trio of North American ‘Buffett/active’ funds control 28.45% of EDP.

Surely the exit plan of these guys must involve selling the whole business.

Maynard