02 January 2026

By Maynard Paton

Apologies! This Q3 2025 update is three months late, but has been published to ensure a complete set of quarterly portfolio reviews is available before I stop blogging about my shares.

A summary of my portfolio’s progress:

- Return for the nine months to 30 September 2025: -21.9%*

- Q3 trades: 1 Top-up (S & U at £18.71).

(*Performance calculated using quoted bid prices and includes all dealing costs, withholding taxes, broker-account fees, paid dividends and cash interest)

What an awful 2025 I am having. During the first nine months of the year, my portfolio has slumped 21.9% while the FTSE 100 has surged 17.7%. I am quite sure this relative performance is the worst I have endured since I started investing 30 years ago.

This year’s woeful return is due entirely to System1, in which I used to have an oversized position because of its multi-bagger potential.

That potential has now all but evaporated as the ad-testing outfit reverted to its former haphazard ways and admitted FY 2026 revenue would remain unchanged less than three months after predicting 15% growth. This business has consistently failed to deliver on its long-term promise, and really should be sold to an organisation capable of fully exploiting its “market-leading platform“.

Newsflow from my other holdings has again been mixed, with a favourable Supreme Court ruling for S & U by far the most promising Q3 event. I am hopeful this specialist lender can now enjoy a few years of undisturbed progress following a protracted period of regulatory and legal disruption.

Elsewhere, the 10% interim dividend lift from M Winkworth was the most encouraging Q3 payout development. I should add System1 actually declared a special dividend alongside its FY 2025 ordinary dividend, although both payments have become somewhat academic in light of the group’s aforementioned warning. Flat dividends at Andrews Sykes, City of London Investment and Mincon were not ideal, but at least this Q3 did not witness any payout reductions.

I have summarised below what happened to my portfolio during July, August and September. (Please click here to read all of my previous quarterly round-ups) .

Contents

Disclosure: Maynard owns shares in Andrews Sykes, Bioventix, City of London Investment, Mincon, Mountview Estates, S & U, System1, FW Thorpe and M Winkworth.

Q3 share trades

S & U

I have increased my S & U (SUS) position by approximately 6% at £18.71 including all costs.

After buying at £14.64 during Q2 ahead of the crucial Supreme Court decision, I was delighted the country’s leading judges decided to overturn an earlier legal verdict — and instead ruled car dealers did not have a “fiduciary duty” towards borrowers and therefore could not be ‘bribed’ by motor-finance lenders.

Following the Supreme Court’s judgment, SUS claimed its motor-finance subsidiary ought to be relatively well placed versus rival lenders hampered by separate compensation claims for discretionary commission arrangements and what the Supreme Court deemed to be “unfair” commissions.

[RNS August 2025]

“Advantage is in the fortunate position of avoiding any redress on DCA-related deals, which it never offered. It is also in a very strong position to disprove any unfair relationship claims under the Consumer Credit Act or Consumer Duty, given the size and proportion of commissions paid relative to the total charge for credit, and its excellent customer relations.”

SUS also provided encouraging commentary about the group’s greater appetite for debt to fund a “revival in growth”:

[RNS August 2025]

“Whilst borrowings at half-year were around £185m against current funding facilities of £280m, the recent revival in growth in both businesses is forecast to generate funding requirements exceeding these within the next two years.”

I bought more simply because I did not believe any “revival in growth” was priced into the shares, which at the time traded approximately 5% below the SUS’s then £19.59 per share net asset value. Read my latest SUS review.

Q3 portfolio news

As usual I have kept watch on all of my holdings. The Q3 developments are summarised below:

- Andrews Sykes: The UK experiencing “one of the driest springs on record” keeping revenue, profit and the dividend all flat during H1 2025.

- Bioventix: Nothing of significance

- City of London Investment: Q4 2025 funds under management suffering a further $198m outflow but positive investment returns lifting FY 2025 earnings per share by 10%.

- Mincon: H1 2025 showing greater construction-related sales pushing total revenue up 9% and “operational and sourcing efficiencies” lifting operating profit to €4m.

- Mountview Estates: Protest votes at what was another lively AGM.

- S & U: A favourable Supreme Court ruling followed by news of motor-finance advances exceeding budget and a welcome “revival in growth” that requires significant extra funding.

- System1: FY 2025 revealing a special dividend alongside Q1 2026 predicting 15% revenue growth for FY 2026, then followed by a bombshell warning predicting unchanged revenue for FY 2026, then followed by a robust AGM.

- FW Thorpe: Nothing of significance.

- M Winkworth: Very mixed H1 2025 numbers showing revenue up 1%, profit down 23% but the dividend up 10%.

Q3 portfolio returns

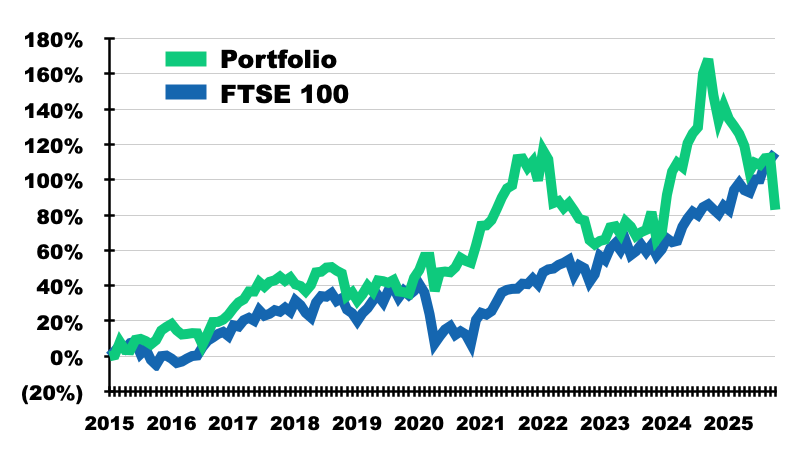

The chart below compares my portfolio’s monthly progress to that of the FTSE 100 total return index:

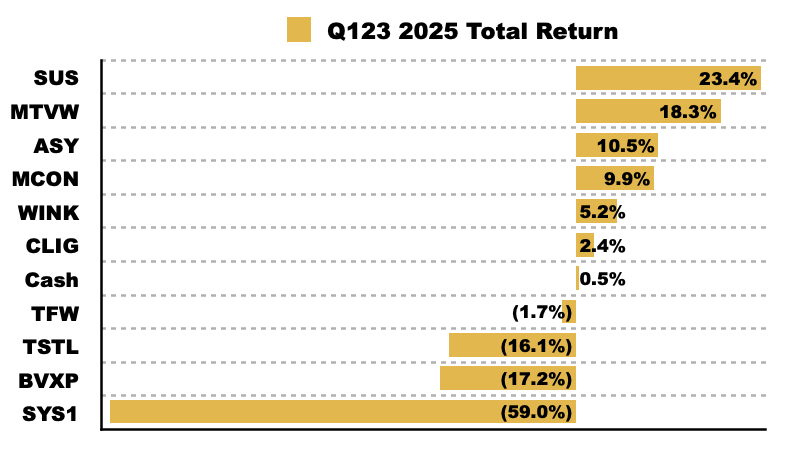

The next chart shows the total return (that is, the capital gain/loss plus dividends received) each holding has produced for me during the first nine months of the year:

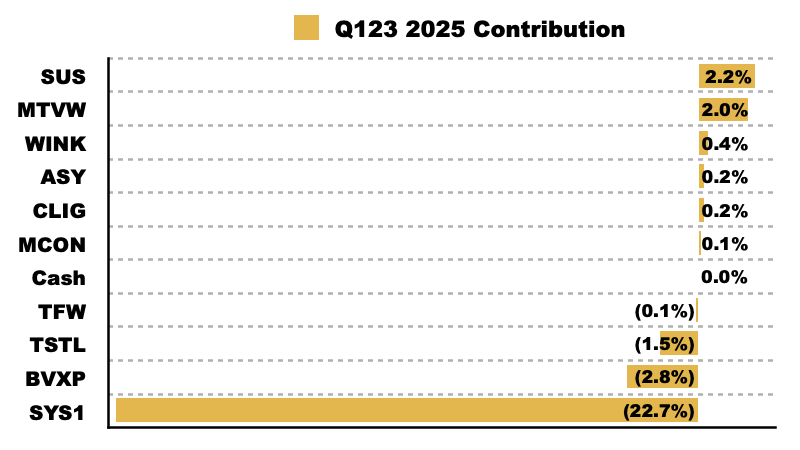

This chart shows each holding’s contribution towards my 21.9% nine-month loss:

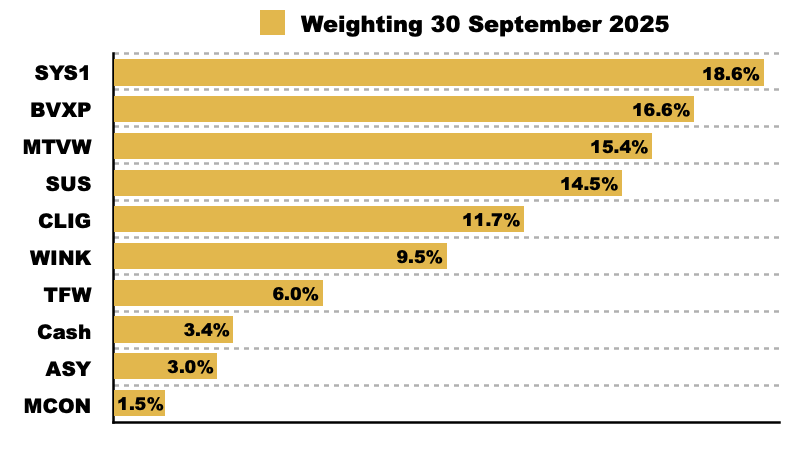

And this chart confirms my portfolio’s holdings and their weightings at the end of Q3 2025:

Maynard Paton